A Prevent365 Risk Advisory Guide for Missouri Business Owners, CFOs, and HR Leaders

Most Missouri businesses carry general liability insurance. Many have an umbrella policy on top of it. A good portion have commercial auto, workers' compensation, and maybe a professional lines policy in the mix. By most appearances, they look covered.

But every year, companies that believed they were adequately protected discover costly exposure in exactly the places they never thought to examine: a subcontractor's lapse, a contract clause they signed without scrutiny, an employment claim they assumed was a management issue, a data breach their GL policy explicitly excludes.

This guide is not about adding more insurance. It is about identifying gaps in your program and understanding why they matter to your bottom line, operations, and long-term business value. These are the questions we hear most often from Missouri business owners, CFOs, and HR leaders. The ten risks below answer them directly.

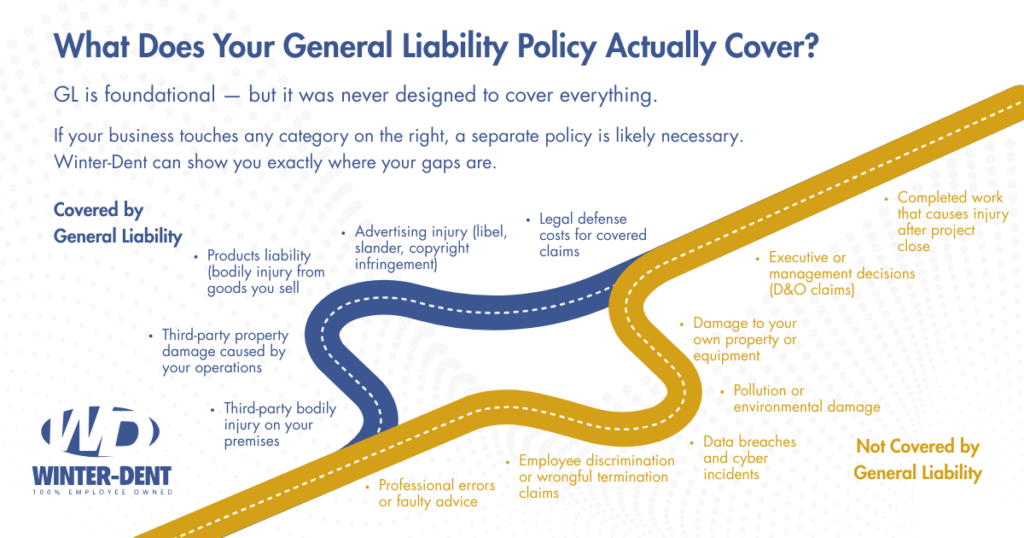

Risk #1: Assuming General Liability Covers Everything

The most common question we hear from business owners evaluating their programs is some version of: "What liability risks am I not thinking about?" The honest answer almost always starts here.

General liability is foundational, but it is not comprehensive. It covers bodily injury and property damage caused by your operations to third parties. It does not cover professional errors, employment disputes, data breaches, pollution events, or damage to your own property.

Missouri business owners often discover these exclusions at the worst possible time: after a claim has been filed. A GL policy that costs $5,000 a year does not protect a $2 million professional services contract, a $500,000 employment lawsuit, or a six-figure cyber incident.

The practical question is not whether you have general liability. It is whether you have identified everything GL does not cover and made a deliberate decision about how to address those gaps.

Prevent365 Perspective: During an annual diagnostic, we map every line of coverage against your actual operations, contracts, and growth plans. Gaps are documented before a claim makes them visible.

Risk #2: Subcontractor Liability Exposure

A question we hear regularly from contractors and service businesses: "Are we exposed through subcontractors?" The answer is yes, and more directly than most business owners realize.

When a subcontractor causes an injury or property damage while working on your project, the injured party may pursue you as the hiring entity, not just the subcontractor. If that subcontractor does not carry adequate insurance, or if their policy lapses mid-project, your business may be left holding the liability.

Missouri courts have consistently applied joint and several liability principles in construction and service contexts, meaning your exposure can extend well beyond your portion of fault. Contract language and certificate management are your primary controls here, not additional premium.

What controls this risk:

- Requiring certificates of insurance from all subcontractors before work begins

- Verifying that those certificates reflect current, not expired, coverage

- Confirming that subcontractor coverage limits are at least equal to your own -- a certificate with inadequate limits provides incomplete protection regardless of additional insured status

- Requiring additional insured status on their policies naming your business, with Additional Insured/Hold Harmless wording included in the actual subcontractor agreement, not just the certificate

- Including indemnification language in all subcontractor agreements that is enforceable under Missouri law

Risk #3: Gaps Between Contracts and Policies

Business owners and CFOs frequently ask: "What gaps exist between our contracts and our policies?" This is the right question, and it rarely gets a thorough answer at renewal time.

Business contracts create obligations that your insurance program may not be designed to fulfill. This mismatch is one of the most overlooked sources of uninsured liability exposure for Missouri companies.

Common scenarios include:

- A service agreement requires you to carry $5 million in professional liability. Your current limit is $1 million.

- A construction contract includes a broad indemnification clause that holds you responsible for incidents partially caused by others.

- A lease agreement requires you to insure the landlord as an additional insured on your GL policy, but the endorsement was never added.

- A government contract requires specific workers' compensation or automobile liability limits that exceed your standard program.

The problem is not that businesses sign these contracts intentionally without coverage. The problem is that contracts are often reviewed by operations or legal, while insurance is managed separately, and the two conversations rarely happen in the same room.

Prevent365 Perspective: Contract review is part of our engagement process, not an add-on. Before a renewal, we ask clients to share new or modified contracts so coverage requirements can be evaluated alongside policy terms.

Risk #4: Cyber Liability Is Excluded From General Liability

"Is cyber really excluded from GL?" Yes. And Missouri businesses are regularly surprised by this. When cyber incidents are excluded from your GL policy, your carrier has no obligation to defend you against related claims -- even if a lawsuit is filed. That distinction matters more than most business owners realize until they need it.

In 2014, Insurance Services Office (ISO) began issuing exclusions that explicitly remove coverage for data breaches and electronic data loss from standard GL policies. Most commercial GL policies issued today include these exclusions as a matter of course. ISO's CG 21 06 endorsement and related forms are now standard language in most carriers' policies. If you have not purchased a standalone cyber liability policy, you are almost certainly uninsured for:

- Notification costs to affected customers or employees following a breach

- Regulatory fines and penalties under state or federal data protection requirements

- Third-party claims from customers or partners whose data was compromised

- Business interruption losses from a ransomware attack or system outage

- Forensic investigation and legal response costs

Missouri's data breach notification law (RSMo 407.1500) requires businesses to notify affected individuals when personal information is compromised. The cost of that notification alone, particularly for companies holding large volumes of customer or employee data, can exceed what most businesses expect. According to IBM's 2025 Cost of a Data Breach Report, notification costs average around $390,000 per incident and that is before factoring in forensic investigation, legal response, or lost business. At the per-record level, customer and employee personal information runs roughly $160 to $168 per compromised record. For a business holding even a few thousand customer or employee records, total breach costs can move well into six or seven figures. U.S. businesses face the highest breach costs of any region, averaging $10.22 million per incident in 2025. Standalone cyber coverage is the appropriate solution, and limits should be sized to reflect the volume and sensitivity of the data your business holds.

Risk #5: Employment Practices Liability Claims Are Rising

"Are EPLI claims increasing?" Yes, and Missouri employers are not insulated from this trend.

Missouri employers face a steady increase in employment-related claims, including wrongful termination, discrimination, sexual harassment, retaliation, and failure to accommodate. None of these are covered under a standard general liability policy. EEOC charge filings have remained elevated nationally, and retaliation claims are now the most frequently filed charge type.

Employment Practices Liability Insurance (EPLI) is a separate line of coverage that most small and mid-size Missouri businesses either do not carry or carry with limits that are inadequate relative to the claims environment.

The claim landscape has shifted. With the expansion of remote work, the formalization of HR documentation requirements, and increased employee awareness of protected class rights, claims that were historically uncommon in smaller businesses are now routine. Missouri's two-year statute of limitations on employment discrimination claims creates a window of exposure that extends well beyond the incident date.

EPLI exposure is not limited to large employers. A 25-person company that terminates an employee without documented performance history carries meaningful risk. A 100-person company without a formal harassment response policy carries more. Businesses without standalone EPLI coverage and without documented HR practices face both insurance and operational exposure.

Risk #6: Your Umbrella Does Not Fill Every Gap

"Does our umbrella fill all gaps?" This is one of the most important misconceptions to address, and the answer is no.

An umbrella policy extends the limits of your underlying liability coverages. What it does not do is create coverage where none exists in the underlying policies. The umbrella follows form, meaning it takes the shape of what is underneath it. Exclusions in underlying policies travel upward.

If your GL policy excludes cyber liability, your umbrella will not cover a cyber claim. If your GL policy excludes professional errors, your umbrella will not respond to a professional liability lawsuit. Additionally, umbrella policies often include their own conditions and exclusions that may not align with your primary policies. Coverage territory, professional services carve-outs, and employment-related exclusions in umbrella forms vary significantly by carrier.

The practical test: if you experienced your worst-case liability scenario tomorrow, would every layer of your program respond as you expect? In most cases, the answer is: not without first verifying the underlying policy language.

Risk #7: Directors and Officers Liability for Privately Held Companies

Many Missouri business owners assume that Directors and Officers (D&O) liability insurance is only relevant for publicly traded companies. This assumption carries significant personal risk.

Private companies face D&O claims from employees, shareholders, creditors, customers, and regulatory agencies. Common claim triggers include:

- Alleged breach of fiduciary duty in business decisions

- Employment disputes escalated to the ownership or board level

- Competitor claims of unfair business practices

- Regulatory investigations into management decisions

- Creditor claims during financial distress or bankruptcy proceedings

Personal assets of directors and officers are not automatically protected by the corporation in many claim scenarios, particularly when plaintiffs allege intentional conduct or personal enrichment. D&O insurance provides defense costs and indemnification that the company's general liability policy does not.

Risk #8: Pollution and Environmental Liability

Missouri's industrial, agricultural, and distribution economy creates meaningful pollution exposure for businesses that may not think of themselves as environmental risk candidates. Standard GL policies include pollution exclusions that can be surprisingly broad.

The pollution exclusion in most GL policies is not limited to industrial facilities or chemical manufacturers. Courts in Missouri have applied pollution exclusions to:

- Carbon monoxide incidents in commercial properties

- Fuel or oil releases from vehicles and storage tanks

- Pesticide or herbicide application in agricultural or landscaping operations

- Mold remediation liability in commercial real estate

- Lead paint claims in renovation and contracting work

If any of your operations involve substances that could be characterized as pollutants under your policy's definition, which is often broader than the regulatory definition, confirm whether your program includes pollution liability coverage or whether you are relying on GL coverage that will not respond.

Risk #9: Liquor Liability and Contingent Alcohol Exposure

Missouri businesses that serve, sell, or provide access to alcohol carry liability exposure that requires separate attention from standard GL. This includes not only bars and restaurants but also businesses that host client events, sponsor community gatherings, or permit alcohol consumption at company-sponsored functions.

Missouri's dram shop law creates potential liability for businesses that serve alcohol to visibly intoxicated persons who subsequently cause injury to others. Standard GL policies commonly exclude liquor liability for businesses where alcohol service is part of regular operations. Even for businesses where alcohol service is incidental, the exclusion may apply depending on policy language.

The risk extends to company events. An employer-sponsored gathering where alcohol is served and an employee subsequently causes an automobile accident creates both direct and contingent liability. This scenario produces claims in Missouri every year and catches business owners off guard because they never thought of their holiday party as a liability event.

Risk #10: Products and Completed Operations Liability for Contractors and Manufacturers

Missouri contractors and manufacturers carry a specific category of liability that standard GL coverage addresses inconsistently: the products-completed operations exposure.

For contractors, this is the liability that arises from work that has been completed and accepted by the client. A building contractor finishes a project; six months later a structural issue emerges and a third party is injured. The claim arises after project completion, potentially outside the policy period in which the work was performed.

For manufacturers and distributors, product liability covers claims arising from bodily injury or property damage caused by products you make, distribute, or sell. Missouri's strict liability doctrine for defective products means that fault is not always required. If a product causes harm, the manufacturer and often the distribution chain may be held responsible.

Key questions for contractors and manufacturers:

- Does your GL policy include products-completed operations coverage with adequate limits?

- Are completed operations limits sufficient relative to the size and type of projects you complete?

- Have you retained completed operations coverage under prior policies for long-tail claims?

- Does your product liability program reflect the actual volume and type of products moving through your distribution chain?

How Winter-Dent Approaches Liability Risk

Winter-Dent & Company is not a transactional insurance broker. Our Prevent365 methodology is built around a core premise: the most valuable thing we do for a client happens before a claim, not after one.

Our liability risk process involves four components:

- Diagnostic Assessment

We begin every engagement by mapping your actual operations, contracts, subcontractor relationships, employee practices, and data exposure against your current program. We document what is covered, what is excluded, and where limits may be inadequate.

- Differentiation to Underwriters

Most insurance buyers are priced on category and claims history alone. We build documented narratives for underwriters that distinguish your business based on management practices, risk controls, and loss prevention investments. Better differentiation produces better pricing and broader coverage terms.

- Contract and Compliance Review

We review contract language before you sign to identify coverage obligations. Certificates of insurance are tracked and verified. Compliance with contractual requirements is confirmed, not assumed.

- Year-Round Engagement

Liability exposure changes as businesses grow, add services, hire employees, take on new clients, and revise contracts. Our Prevent365 model keeps your program aligned with your actual risk profile throughout the year, not just at renewal.

Start With a Liability Risk Review

If your business operates in Missouri and you have not had an independent review of your liability program in the past 12 months, there is a meaningful probability that one or more of the risks described above exists in your current program. Winter-Dent & Company offers a no-obligation Prevent365 diagnostic for Missouri businesses. Contact us to schedule your review.