You've invested in safety training. You've implemented a robust return-to-work program. You've reduced your incident rate over the past two years. Your leadership team is deeply committed to workplace safety and risk management.

But when renewal time comes, your insurance premium still increases. Your carrier treats you like every other company in your industry. Your rates reflect industry averages rather than your actual performance.

Why? Because your underwriter doesn't know what makes you different.

Traditional insurance processes lump companies together based on industry codes and basic metrics. Your proactive efforts, safety culture, and risk management excellence remain invisible to the carriers making pricing decisions.

At Winter-Dent, our Prevent365 program changes this dynamic. We help you de-average your company by strategically documenting and showcasing what makes you a better-than-average risk.

The result: better pricing, improved terms, and access to preferred markets.

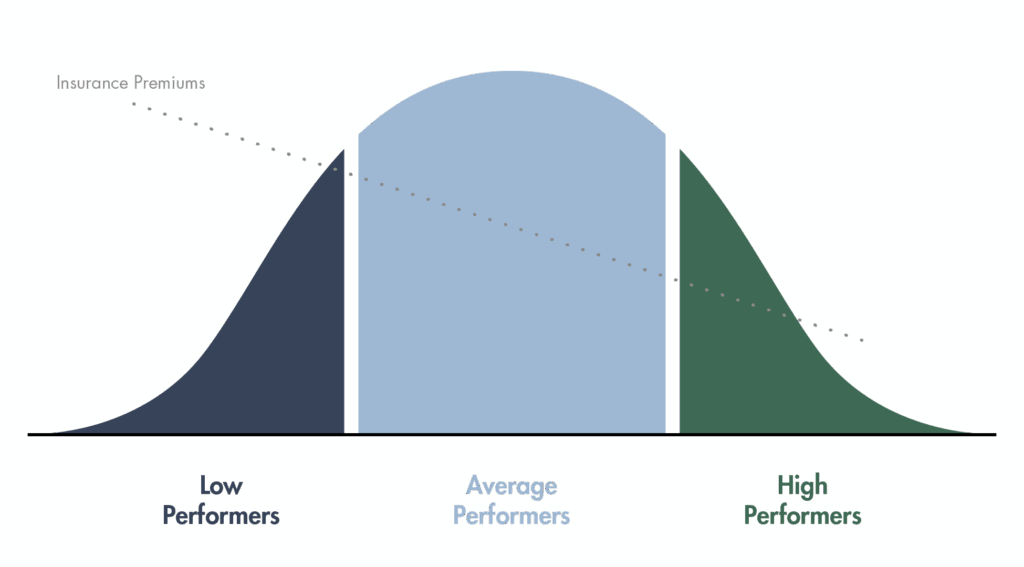

The Problem: Why Average Companies Get Average Treatment

The insurance industry runs on classification systems designed for efficiency, not accuracy. When underwriters evaluate your business, they start with broad industry categories and basic data points.

How Underwriters See Your Business (Without Differentiation)

- Industry Classification Code: This four to six-digit code groups you with thousands of other businesses in similar industries. A manufacturing company gets coded as "manufacturing." A construction firm gets coded as "construction." The nuances of your specific operations, safety culture, and risk controls are invisible.

- Basic Metrics: Underwriters see your revenue, employee count, claims history, and experience modification rate. These numbers tell part of the story, but they don't reveal the investments you've made in prevention or the improvements you've implemented.

- Historical Loss Data: Your past claims appear as line items on a loss run. The circumstances, root causes, and corrective actions you took afterward are unknown to the underwriter reviewing your account.

- Standard Application Information: The insurance application captures basic operational details but doesn't provide space to showcase your safety initiatives, compliance programs, or risk management philosophy.

What Gets Lost in Translation

This standardized approach means critical differentiators never reach the underwriters making pricing decisions:

- Your proactive safety initiatives like weekly safety meetings, comprehensive new-hire training programs, or regular equipment maintenance schedules go unnoticed.

- Your investment in workers comp safety programs including automated training systems, OSHA recordkeeping tools, and return-to-work protocols isn't valued.

- Your strong leadership commitment demonstrated through safety committee participation, capital investment in risk controls, and employee engagement efforts remains invisible.

- Your documented improvements showing incident rate reductions, claims cost decreases, and experience mod trends in the right direction aren't properly presented.

- Your culture of safety and compliance built over years of consistent effort and reinforcement doesn't translate into underwriting data.

The Costly Result

When underwriters can't see what makes you different, they default to industry averages. You're priced alongside companies that haven't made your investments in safety and risk management. You pay more than you should, get fewer coverage options, and miss opportunities for better terms.

Even worse, companies with poor safety records benefit from this averaging effect. They get better rates than their actual risk warrants because they're pooled with better performers like you.

The Prevent365 Approach to Differentiation

Winter-Dent's Prevent365 process transforms you from an anonymous account number into a compelling risk story that underwriters can't ignore.

Strategic Positioning vs. Simple Submission

Traditional agents complete applications and submit them to multiple carriers. They "spray and pray," hoping someone offers a decent rate. Then they present you with options and move on to the next account.

We take a fundamentally different approach:

- Strategic Documentation: We systematically document your risk management excellence, creating a comprehensive profile that goes far beyond standard applications.

- Targeted Marketing: Rather than blanket submissions, we identify carriers whose appetite and underwriting philosophy align with your risk profile.

- Active Advocacy: We don't just submit your information. We actively sell your story to underwriters, highlighting the specific factors that make you a preferred risk.

- Compelling Presentation: We present your business in the most favorable light, using data and documentation that demonstrate measurable safety improvements and proactive risk management.

Building on Your Assessment Findings

The differentiation process builds directly on the Prevent First Assessment. Those findings provide the foundation for positioning your business effectively.

- Identified Strengths Become Differentiators: The positive initiatives we documented during your assessment become proof points for underwriters. Your return-to-work program isn't just mentioned; it's quantified with metrics showing reduced lost-time days and claim costs.

- Improvements Show Commitment: Changes you've implemented based on assessment findings demonstrate that you're serious about risk management, not just insurance shopping.

- Data Tells Your Story: The trends we identified in your loss runs, OSHA logs, and safety metrics provide compelling evidence of your risk management trajectory.

- Documentation Creates Credibility: Rather than making claims about your safety culture, we provide concrete evidence through policies, procedures, training records, and compliance documentation.

Key Differentiators That Underwriters Value

Not all differentiators carry equal weight with underwriters. Through years of experience, we know which factors move the needle on pricing and terms.

#1 Documented Safety Programs

Underwriters want to see comprehensive, actively used safety programs, not binders gathering dust on shelves.

What makes a safety program impressive to underwriters:

- Written safety policies tailored to your actual operations (not generic templates)

- Regular safety committee meetings with documented minutes and action items

- Incident investigation protocols that identify root causes and corrective actions

- New hire safety orientation programs with sign-off documentation

- Regular safety training with attendance records and competency verification

- Hazard identification and correction procedures actively used by employees

- Emergency response plans tested through regular drills

We help you document these elements in ways that underwriters can quickly understand and value.

Tool spotlight: Companies using OSHAlogs for OSHA recordkeeping and AutomateSafety for training deployment can provide concrete documentation of their safety program effectiveness.

#2 Claims Management Excellence

How you handle claims matters as much as claim frequency. Underwriters look for businesses that actively manage incidents to minimize severity and duration.

Effective claims management includes:

- Return-to-Work Programs: Structured programs that get injured employees back to productive work quickly (even in modified duty) dramatically reduce claim costs. Companies using LightDutyWorks can demonstrate systematic return-to-work processes with measurable results.

- Prompt Reporting: Claims reported within 24 hours have better outcomes than those reported days later. We document your reporting protocols and compliance rates.

- Investigation and Follow-Up: Root cause investigations that lead to corrective actions show underwriters you're preventing future incidents, not just paying for past ones.

- Claims Trend Analysis: Understanding your claims patterns through ModSure insights helps you manage the factors impacting your experience modification rate. We present this data to show you're actively managing your mod.

- Medical Management: Relationships with preferred providers, nurse case management, and fraud prevention measures all signal sophisticated claims management.

#3 Culture and Leadership Commitment

Underwriters increasingly recognize that strong safety cultures prevent incidents more effectively than any single program or policy.

Demonstrating cultural commitment includes:

- Management Participation: Leadership actively participating in safety initiatives (not just delegating to a safety officer) sends a powerful signal.

- Employee Engagement: High participation rates in safety committees, training programs, and hazard reporting systems indicate cultural buy-in.

- Investment Evidence: Capital investments in safety equipment, facility improvements, and technology tools demonstrate commitment beyond words.

- Communication Systems: Regular safety communications, toolbox talks, and feedback mechanisms show ongoing focus on safety.

- Recognition Programs: Safety incentive programs that reward safe behaviors (not just lack of incidents) build positive culture.

#4 Process and Compliance Excellence

Solid operational processes and regulatory compliance demonstrate organizational maturity and reduced risk.

Process excellence indicators include:

- HR Policies and Handbooks: Well-crafted employee handbooks that set clear expectations, comply with regulations, and protect the company from liability while being fair to employees.

- Compliance Management: Systematic compliance tracking using tools like ComplianceCheck ensures you stay ahead of OSHA and other regulatory requirements across multiple jurisdictions.

- Vendor Management: Procedures for vetting subcontractors, monitoring their safety performance, and ensuring they carry adequate insurance.

- Standard Operating Procedures: Documented processes for high-risk activities that ensure consistency and safety.

- Quality Control: Systems that prevent errors and defects reduce both operational and liability risks.

- Cyber Security: In an increasingly digital world, documented cyber security measures (employee training, technical controls, incident response plans) show you're managing emerging risks.

How We Position Your Business to the Market

With differentiators documented, we develop a strategic approach to marketing your business to carriers.

Strategic Marketing vs. Submit and Quit

Traditional agents complete applications and submit them to multiple carriers, hoping someone offers a decent rate. They present you with options and move on to the next account.

We take a fundamentally different approach. We position your business strategically in the marketplace, highlighting the differentiators that matter to underwriters. We actively advocate for your business, ensuring carriers understand your unique value proposition and risk management commitment.

Rather than simply submitting applications, we present your story in a way that showcases what makes you a better-than-average risk. We market and place your coverage with purpose, aggressively representing your risk profile.

This strategic positioning helps carriers see documented evidence of your risk management excellence, leading to better pricing, improved terms, and enhanced market access.

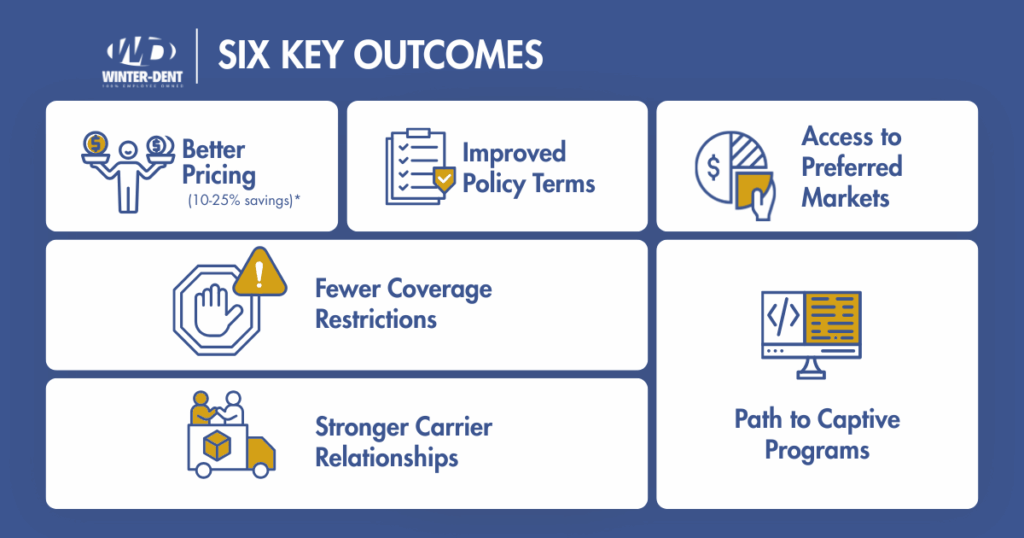

The Results: What Differentiation Achieves

When you effectively differentiate your business, the benefits extend far beyond modest premium savings.

#1 Better Pricing and Premium Reductions

The most obvious benefit is more competitive pricing. When underwriters see documented evidence of your risk management excellence, they price you more favorably than industry averages warrant.

Businesses that successfully differentiate often see premium reductions of 10-25% compared to market averages, even when they've previously had "competitive" rates.

#2 Improved Policy Terms and Conditions

Beyond price, differentiation often leads to better policy terms:

- Lower deductibles or higher limits at competitive pricing

- Broader coverage with fewer exclusions

- More flexible policy terms that better fit your operations

- Better loss-sensitive programs (like dividend plans or retrospective rating)

- Multi-year rate guarantees providing cost stability

#3 Access to Preferred Markets and Programs

Strong risk profiles open doors to markets and programs not available to average risks:

- Preferred Tier Pricing: Many carriers have preferred tiers with significantly better rates for businesses that meet specific criteria. Differentiation helps you qualify.

- Specialty Programs: Industry-specific programs designed for well-managed companies often offer better coverage and pricing than standard markets.

- Alternative Risk Financing: Companies with strong risk management programs may qualify for advanced solutions like commercial comp captive programs or group captive insurance, offering even greater control and potential long-term savings.

- Direct Carrier Access: Top-performing risks sometimes gain access to direct relationships with carriers, bypassing standard market channels.

#4 Fewer Coverage Restrictions and Exclusions

Well-differentiated businesses face fewer coverage restrictions. Underwriters are more comfortable providing broad coverage when they trust your risk management capabilities.

This means:

- Fewer operations excluded from coverage

- Less restrictive policy language

- More flexibility in coverage terms

- Better claims handling and partnership

#5 Stronger Carrier Relationships and Stability

When carriers view you as a preferred risk, the relationship changes. You're not just another account to manage but a valued client they want to retain.

Benefits of preferred status:

- Improved service and responsiveness

- More proactive risk management support from carrier loss control

- Greater stability (less likely to be non-renewed in hard markets)

- Better partnership during claims

- Access to carrier resources and expertise

Real-World Example: De-Averaging in Action

Let's look at how differentiation works in practice with a hypothetical scenario.

The Setup: Two Similar Companies

Company A and Company B:

- Both are regional manufacturing companies

- Both have 150 employees

- Both operate in the same industry classification

- Both have similar revenue ($20M annually)

- Both have three-year loss ratios around 55%

On paper, these companies look nearly identical to underwriters.

Company A: Traditional Approach

Company A's agent completes standard applications and submits to multiple carriers. The submission includes:

- Basic application information

- Loss runs showing claims history

- Experience mod (currently 1.05)

- No additional documentation

Underwriter perspective: Generic manufacturing risk, slightly above-average mod, typical claims history. Price accordingly at market rates.

Result: Quoted premium of $285,000 with standard terms.

Company B: Prevent365 Differentiation Strategy

Company B works with Winter-Dent and provides comprehensive differentiation:

What makes Company B different:

- Completed Prevent First Assessment identifying and addressing key risks

- Implemented structured return-to-work program reducing lost-time claims by 40%

- Deployed AutomateSafety training system with 98% completion rates

- Uses OSHAlogs for proactive OSHA compliance and trend identification

- Management actively participates in monthly safety committee meetings

- Invested $150,000 in ergonomic improvements over past two years

- Achieved 30% reduction in incident rate over three years

- Experience mod trending down (1.05 → 0.98 projected)

Presentation includes:

- Comprehensive safety program documentation

- Claims trend analysis showing improvements

- Training records and completion rates

- Photos of facility improvements and safety controls

- Management commitment letter outlining ongoing initiatives

- Employee engagement metrics

- Third-party safety audit results

Underwriter perspective: Above-average risk with strong safety culture, proactive management, measurable improvements, and documented controls. This is a preferred risk.

Result: Quoted premium of $215,000 (24% savings vs. Company A) with:

- Lower deductibles

- Dividend plan with potential return of 10-15% of premium

- Three-year rate guarantee

- Broader coverage with fewer exclusions

The Competitive Advantage

Company B's lower insurance costs free up $70,000 annually that Company A must spend on insurance. Over three years, that's $210,000 in direct savings, plus potential dividend returns.

But the advantage goes beyond premium dollars. Company B has:

- Fewer incidents disrupting operations

- Better employee morale and retention

- Stronger reputation with customers

- More financial resources for growth and investment

- Foundation for even more advanced risk financing options

That's the power of effective differentiation.

Beyond Traditional Markets: The Path to Advanced Risk Financing

Strong differentiation doesn't just improve your results in traditional insurance markets. It can open doors to sophisticated risk financing alternatives that offer even greater control and potential savings.

Commercial Captive and Group Captive Insurance

For businesses with mature risk management programs, commercial captive programs and group captive insurance offer alternatives to traditional guaranteed-cost coverage.

What are captives?

Captives are insurance companies owned by the insured businesses themselves (or groups of insured businesses). They provide more control over coverage, claims, and pricing while offering potential profit-sharing if claims performance is favorable.

Prerequisites for captive consideration:

- Strong safety culture and documented programs

- Consistent risk management performance

- Leadership commitment to continuous improvement

- Financial stability to handle captive capitalization

- Willingness to invest in prevention

- Track record of claims management excellence

The differentiation work you do through Prevent365’s Differentiate Your Business builds the foundation for captive eligibility. You're documenting the risk management capabilities that captive managers look for.

Benefits of captive participation:

- Greater control over insurance costs and coverage

- Potential for profit sharing and dividends

- Long-term cost stability

- Alignment with other high-performing companies

- Direct involvement in claims and safety decisions

- Customized coverage meeting your specific needs

Not every business is a good fit for captives, but for those that are, the potential benefits are significant. Effective differentiation is the first step toward qualifying.

Ready to Stand Out?

Your business isn't average. Your commitment to safety, your investment in risk management, and your results prove it. But if underwriters can't see what makes you different, you'll keep paying average prices (or worse) for insurance.

Differentiating your business with Prevent365 changes that equation. Through strategic documentation, targeted marketing, and active advocacy, we help you de-average your company and secure the pricing, terms, and market access your performance deserves.

The process builds on the foundation created during our Prevent First Assessment. Those findings become the proof points that differentiate you from competitors and position you as a preferred risk.

From there, we move to the next phase of Prevent365, Go Beyond the Policy, where we implement non-insurance risk controls to protect what insurance can't cover, and to the final phase, Build for Impact, where we create lasting organizational resilience.

But differentiation is the bridge between understanding your risks and actually improving your insurance outcomes. It's where documentation becomes dollars and positioning creates possibilities.

Ready to show underwriters what makes your business different? Let's build your differentiation strategy and secure the insurance outcomes your performance deserves.