Most businesses treat renewal as a deadline. The ones that consistently control costs treat it as a process.

If you are waiting for your broker to call you 30 days before your policy expires, you have already lost most of your negotiating leverage. Commercial insurance is priced on risk perception, and the underwriters writing your coverage are forming opinions about your business long before they see your renewal application.

The business owners who win at renewal are not necessarily the ones with the cleanest loss histories. They are the ones who show up prepared, present their risk story compellingly, and give their broker the tools to differentiate them from every other account in the underwriter's stack.

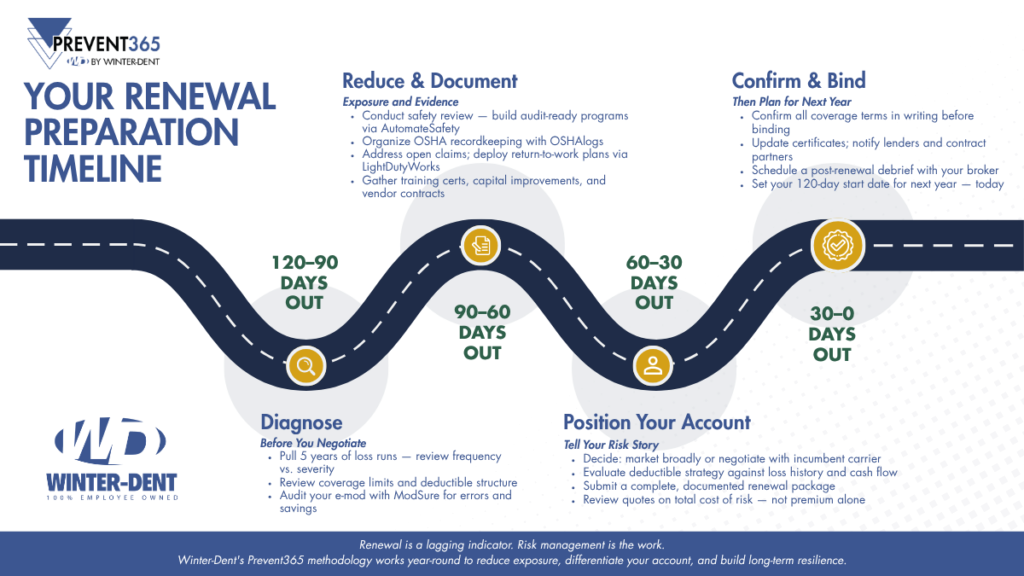

That is the core principle behind Winter-Dent's Prevent365 methodology. Rather than treating renewal as a single event, we treat it as a year-round process of exposure reduction, documentation, and proactive positioning. Here is how that process maps to the 120 days before your renewal date.

| Why 120 Days? Underwriters reward preparation they can verify. Waiting until 30 days out limits your ability to make meaningful operational improvements, gather documentation, explore market alternatives, or negotiate structural changes like deductible strategy. Starting at 120 days gives you time to actually move the needle, not just fill out paperwork. |

Days 120 to 90: Diagnose Before You Negotiate

Before you can improve your insurance positioning, you need an honest picture of where you stand. This phase is about diagnosis, not action.

Pull your loss runs and read them critically

Request five years of loss runs across all lines. Do not just look at totals. Look at frequency versus severity, open reserves, and whether claims show a pattern. Underwriters will see all of this, and you need to understand it before they do. If there are patterns, your broker should be helping you build a narrative that explains root causes and what you have done to address them.

Review your current coverage structure

Are your limits keeping pace with actual exposure? Are your deductibles optimized for your cash flow and risk tolerance, or are they just where they have always been? This is also the time to revisit property valuations. Underinsured property is one of the most common and costly surprises in a loss, and inflated replacement cost assumptions drive unnecessary premium.

Benchmark your experience modification factor

For businesses with workers' compensation exposure, your experience modification factor (e-mod) has a direct and compounding effect on your premium. Winter-Dent uses ModSure to audit e-mod calculations for errors, which are more common than most business owners realize, and to model how future claim outcomes will affect your rating. If your e-mod has room to improve, the time to understand why is now, not at renewal.

For operations with commercial auto or fleet exposure, underwriters also look beyond the mod. The FMCSA's Safety and Fitness Electronic Records (SAFER) system provides carriers and underwriters with a company snapshot that includes safety ratings, inspection histories, and crash data. A poor SAFER profile can affect your insurability and pricing independently of your e-mod. Similarly, the age and maintenance history of your buildings, equipment, and vehicles signal risk condition to underwriters even when your loss history looks clean. Winter-Dent evaluates these factors as part of a complete risk picture, not just at renewal.

Days 90 to 60: Reduce Exposure and Document It

This is the phase where real differentiation happens. Underwriters price risk based on what they believe about your operation. Your job is to give them verifiable evidence that your business is better managed than what the averages suggest.

Conduct a formal safety and compliance review

Underwriters place significant weight on whether your safety programs are documented and consistently applied. Winter-Dent's AutomateSafety platform helps clients build and maintain safety programs that are audit-ready, and OSHAlogs provides accurate, organized OSHA recordkeeping that demonstrates regulatory compliance without the manual burden. These tools matter at renewal because they produce the kind of evidence an underwriter can point to when justifying a favorable rate.

Address open claims strategically

Open reserves sit on your loss runs and signal ongoing exposure. Work with your broker and claims team to understand whether any open claims can be moved toward resolution before your renewal submission. Even where closure is not possible, a documented return-to-work plan or medical management update can positively influence how an underwriter interprets the reserve. LightDutyWorks supports structured return-to-work programs that close claims faster and reduce the total cost of workers' compensation injuries.

Gather documentation that tells your story

Collect certificates of training, safety committee meeting records, capital improvement projects, vendor contracts with solid indemnification language, and any certifications relevant to your industry. The goal is a renewal submission that does not leave an underwriter guessing. Every question they have to ask is an opportunity for the rate to go the wrong direction.

Days 60 to 30: Position Your Account in the Market

With a solid foundation in place, your broker should now be taking your story to market. This is where the work of the previous two phases either pays off or does not.

Evaluate whether to market broadly or stay with incumbent carriers

Not every renewal benefits from a full market submission. Sometimes the best outcome is a well-negotiated renewal with your existing carrier. Other times, introducing competitive tension is the right move. Your broker should be helping you think through this strategically, not just sending your account to every market available.

Have a deductible strategy conversation

Deductible structure is one of the most underutilized levers in commercial insurance. Increasing your deductible on lines where your loss history is strong can produce meaningful premium reduction. The right answer depends on your cash flow, your claims pattern, and your appetite for retained risk. This conversation belongs at 60 days out, not the week of renewal.

Review quotes with total cost of risk in mind

When quotes come in, the premium number is only part of the picture. Evaluate carrier financial strength, claims handling reputation, coverage terms and conditions, and any exclusions that may have shifted from your current policy. A lower quote with narrower coverage is not always a better deal.

Days 30 to 0: Confirm, Bind, and Plan Ahead

The final 30 days should feel like a confirmation, not a scramble. If you have followed the process, the decisions are largely made by now.

- Confirm all coverage terms in writing before binding. Verbal agreements do not hold.

- Update certificates of insurance and notify any lenders or contract partners who require evidence of coverage.

- Schedule a post-renewal debrief with your broker. What worked? What carrier feedback did you receive? What should you be doing differently over the next 11 months?

- Set your 120-day preparation date for next year. Today.

Renewal Is a Lagging Indicator. Risk Management Is the Work.

The businesses that see consistent, predictable insurance costs are not lucky. They have built operating environments that genuinely reduce risk, and they have a broker who knows how to communicate that value to the market.

Winter-Dent's Prevent365 approach is built around the idea that renewal preparation is not a 120-day project. It is a year-round discipline that makes the 120-day window far more effective. If your current broker relationship only activates at renewal time, that is a meaningful gap in your risk strategy.

If you would like to walk through where your business stands today relative to your next renewal, we are glad to start that conversation.

Frequently Asked Questions About Commercial Insurance Renewal

How do we lower our premium before renewal?

The most reliable way to lower your premium is to reduce your actual risk exposure and document it in a way underwriters can verify. That means addressing open claims, strengthening your safety programs, reviewing your experience modification factor for errors, and giving your broker a complete picture of the improvements you have made. Premium is a reflection of how an underwriter perceives your risk. Change the perception by changing the reality, and bring the evidence to support it.

What documents should we have ready?

At minimum: five years of loss runs across all lines, your current policy declarations pages, a list of any capital improvements or operational changes made in the past year, employee safety training records, OSHA logs, certificates of any relevant industry certifications, and vendor contracts that include indemnification language. The more complete your submission, the fewer questions an underwriter has to ask. Unanswered questions rarely move rates in your favor.

When should we start shopping?

Sixty days before renewal is the earliest most markets will engage seriously with new submissions. But if you want to be in a position to shop effectively, the preparation work starts at 120 days out. Showing up at 60 days with clean documentation, a strong loss history narrative, and a well-organized submission is what creates competitive tension. Showing up at 30 days with whatever you can pull together typically just creates stress.

Should we get updated property valuations?

Yes, and most businesses are overdue on this. Construction costs have risen significantly in recent years, and replacement cost valuations that were accurate three or four years ago are often understated today. Underinsured property is one of the most common and costly surprises at the time of a loss. An updated appraisal also gives your broker accurate data to present to underwriters, which avoids both gaps in coverage and the premium waste that comes from insuring an inflated figure.

How do loss runs impact renewal negotiations?

Loss runs are the primary lens underwriters use to evaluate your account. They are looking at two things: frequency and severity. A single large claim is often viewed differently than a pattern of small, recurring losses. Frequency signals a systemic problem in a way that one significant event does not. If your loss history has blemishes, your broker should be helping you build a written narrative that explains what happened, what changed, and why the exposure is different today. Loss runs without context leave underwriters to draw their own conclusions.

What improvements actually influence pricing?

Underwriters respond to changes that reduce the likelihood or severity of a claim. On the property side, roof replacements, updated electrical and HVAC systems, and fire suppression upgrades tend to move the needle. On the liability and workers' compensation side, documented safety training programs, return-to-work policies, and consistent OSHA recordkeeping all signal a well-managed operation. The key word is documented. Improvements that exist only in practice and not on paper are much harder for your broker to leverage in negotiations.

Can we change deductible strategy at renewal?

Yes, and renewal is exactly the right time to have that conversation. Deductible structure is one of the most underused levers in commercial insurance. If your loss history on a given line is strong, increasing your deductible can produce meaningful premium savings that over time outpace the increased retained exposure. The right answer depends on your cash flow, your claims pattern, and your risk tolerance. This is a strategic conversation, not a form to fill out, and it belongs at 60 days out, not the week you are binding.