A CFO's Guide to Healthcare Captives and Why the Right Risk Advisor Makes All the Difference

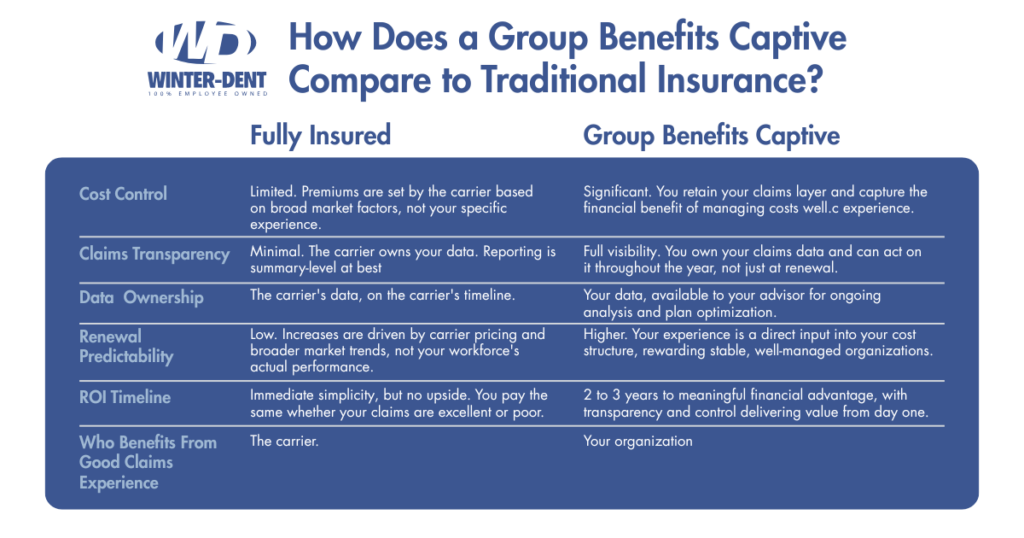

Healthcare costs are one of the most significant and least predictable line items on a company's balance sheet. For many mid-size and larger employers, the traditional fully-insured model offers simplicity but at a steep price: you absorb every carrier rate increase, you have no visibility into your actual claims data, and you have virtually no leverage at renewal.

Group benefits captives, particularly healthcare captives, offer a fundamentally different approach. Rather than transferring all risk and all potential savings to an insurance carrier, a captive allows your organization to retain a portion of your healthcare risk, pool intelligently with similar employers, and capture the financial upside of keeping your workforce healthy.

But is a captive right for your organization? That depends on several factors that go beyond premium volume alone.

At Winter-Dent & Company, our Prevent365 methodology is built on understanding what's driving healthcare spend before designing a solution. When it comes to employee benefits, that means helping clients understand what's actually driving their healthcare spend and whether a captive structure would give them more control, more transparency, and better long-term economics.

Here are five signs a group benefits captive may make financial sense for your organization.

Sign #1: You're Paying for Predictability You're Not Getting

The promise of a fully-insured health plan is straightforward: pay a fixed premium, transfer the risk, avoid surprises. In practice, many employers find that promise hollow. Renewal increases of 15 to 25 percent are common, not because your claims were bad, but because the carrier is pricing for the broader market, not your workforce.

If your organization has relatively stable, manageable claims history and you're still experiencing significant year-over-year premium increases, you may be subsidizing other employers' poor outcomes.

A group benefits captive changes that equation. By retaining your layer of predictable claims, typically called the "working layer," you stop paying the carrier's profit margin and administrative load on dollars you could be self-funding. Stop-loss coverage protects you against catastrophic claims, and the captive layer pools aggregate risk with peer organizations, giving you the best of both worlds: control and protection.

The CFO question to ask: "How much of our premium increase is based on our actual claims experience and how much is market-driven?"

Sign #2: You Want Transparency Into What's Driving Your Costs

In a fully-insured arrangement, your claims data belongs to the carrier. You may receive some summary reporting, but granular visibility into cost drivers, including chronic condition prevalence, high-cost claimants, pharmacy spend, and utilization patterns, is often limited or unavailable.

Without data, you can't manage costs. You can only react to them at renewal.

Group benefits captives typically operate on a self-funded chassis, which means your organization has access to real claims data. That data becomes a strategic asset. It allows your advisor to identify trends early, deploy targeted wellness or care management programs, and address root causes of spend before they compound into a renewal crisis.

This is precisely the kind of insight that separates a strategic risk advisor from a policy vendor. If your broker isn't bringing you data-driven analysis between renewals, you're experiencing a service gap, not a service relationship.

The CFO question to ask: "Do we have enough claims transparency to actually manage our healthcare costs, or are we flying blind until renewal?"

Sign #3: Your Workforce Is Relatively Stable, and You Invest in Health

Captives reward employers who are intentional about workforce health. If your organization has implemented wellness programs, care navigation, chronic disease management, or pharmacy benefit strategies, a captive allows you to financially benefit from those investments rather than contributing those gains to a carrier's underwriting pool.

In a captive structure, favorable claims experience flows back to your organization or reduces your future contributions, rather than being pooled anonymously with thousands of other employer groups.

Conversely, employers with high turnover, volatile workforce demographics, or limited appetite for health management may find the captive model less advantageous. The structure rewards intentionality, and that's by design.

The CFO question to ask: "Are we doing the things that should produce better-than-average claims outcomes and are we capturing any financial credit for it?"

Sign #4: You Don't Have to Be a Fortune 500 to Qualify

One of the most common misconceptions about captives is that they're exclusively for large enterprises. That was largely true a decade ago. It's not the landscape today.

Group captives, sometimes called association captives or consortium captives, have dramatically lowered the entry point by allowing multiple mid-size employers to pool together within a shared captive structure. Each member retains their own working-layer risk but shares aggregate stop-loss capacity and captive infrastructure costs.

As a general benchmark, Winter-Dent looks for organizations with 50 or more benefits-eligible employees, consistent annual health premium spend above $250,000, and a stable loss history. Equally important are factors that don't show up on a spreadsheet: a genuine commitment to wellness and proactive risk management, and the financial stability to share in risk over time. For organizations that meet those criteria, a healthcare captive can deliver substantial economic advantages while providing far greater control and transparency than a traditional fully-insured program ever would.

The more meaningful threshold isn't headcount, it's claims credibility. Underwriters and captive managers want to see enough claims history to distinguish your experience from statistical noise. Generally, three to five years of stable loss data positions an employer strongly for captive consideration.

The CFO question to ask: "Are we large enough and do we have enough claims history to be meaningfully differentiated in a captive structure?"

Sign #5: You're Willing to Think About the Next Three to Five-Years, Not Just Annual Renewals

Captives are not a short-term arbitrage play. The economics build over time. In year one, you're establishing the structure, funding appropriate reserves, and gaining claims visibility. By years two and three, you're seeing the data dividend, the ability to intervene, adjust plan design, and deploy targeted programs. By years three through five, well-run captives typically demonstrate meaningful financial advantages over fully-insured benchmarks.

Organizations that chase the cheapest fully-insured renewal every year, switching carriers for a one-time discount, rarely build the claims history or carrier relationships that make alternative structures viable. Stability and intentionality compound.

This is also where advisor continuity matters enormously. A captive isn't a product you purchase once. It requires ongoing actuarial analysis, stop-loss negotiations, claims data review, regulatory compliance, and plan design optimization. The advisor who places you in a captive needs to be genuinely engaged year-round, not just at renewal.

The CFO question to ask: "Are we managing our benefits program as a strategic, multi-year initiative or are we making reactive, transactional decisions every 12 months?"

How Long Before We See ROI?

This is the question every CFO asks, and it deserves a candid answer.

Most employers in well-structured group captives begin to see financial advantages within two to three years. The trajectory depends on claims experience relative to the group, investment in health management programs, the quality of stop-loss coverage and captive management, and how actively the advisor engages in ongoing plan optimization.

The ROI isn't purely financial either. Transparency, control, and the ability to make data-informed decisions have strategic value that compounds even in years where claims run higher than expected.

That said, captives are not appropriate for every organization. If your healthcare claims history is volatile, your workforce demographics are shifting significantly, or your leadership isn't prepared to engage with the data and management responsibilities a captive requires, a fully-insured or traditional self-funded arrangement may serve you better for now. A captive is the right fit for the right organization with the right advisor at the right time.

The Service Problem No One Talks About

There's a structural issue in the group benefits space that deserves direct attention: most employers don't have a strategic advisor. They have a policy vendor.

The symptoms are recognizable. You only hear from your broker at renewal. Your renewal arrives as a surprise, with no early warning, no strategy conversation, and no market positioning work done in advance. You have no claims data or analysis, so you're making plan design decisions without the underlying information to support them. Costs keep rising, and the only explanation you receive is that the market is up. And no one has ever discussed a captive, not because it isn't appropriate, but because the broker doesn't have the capability or the incentive to bring it up.

These aren't minor inconveniences. They're symptoms of a transactional relationship masquerading as an advisory one.

If you only hear from your broker when your renewal is due, you aren't being served. You're being overlooked.

The Prevent365 Difference

Winter-Dent's Prevent365 methodology was built around a simple premise: risk management is a 365-day discipline, not an annual event.

In the group benefits context, that means diagnosing cost drivers before they become renewal surprises, differentiating your organization to captive managers and stop-loss underwriters based on the strength of your health management programs, reducing exposure by identifying and addressing what's actually driving your claims, and building long-term financial resilience through structures, including captives, that create durable competitive advantages.

If your current advisor isn't bringing you this kind of engagement, it may be time for a service audit.

Is a Group Benefits Captive Right for You?

Every organization's situation is different. A rigorous captive feasibility analysis should include a historical claims experience review covering three to five years, a workforce demographic and stability assessment, an evaluation of your current plan design and carrier relationships, stop-loss market analysis, a captive structure comparison across group, single-parent, and association options, and multi-year financial modeling under multiple claims scenarios.

This is the kind of analysis Winter-Dent performs as part of our benefits advisory process, not as a sales exercise but as a diagnostic one. The right answer for your organization may be a captive, a traditional self-funded program, or a fully-insured arrangement with better market representation. Our job is to help you find that answer with clarity and confidence.

Ready to find out if a group benefits captive makes sense for your organization?

Contact Winter-Dent & Company to schedule a benefits strategy conversation. We'll start with the data, ask the right questions, and give you an honest picture of your options and your opportunity.

Winter-Dent & Company is an employee-owned insurance and risk management firm. Our Prevent365 methodology is designed to help business owners, CFOs, and HR leaders move from reactive insurance buying to proactive benefits management.