Every general contractor eyeing larger projects eventually hits the same wall: "We need bonding capacity." But here's what most don't realize until they're deep into the process: getting bonded isn't just about having enough working capital on your balance sheet.

Sureties make a three-party promise: If you can't complete a project, they'll step in to ensure the owner doesn't suffer. That means they're not just looking at your financials. They're evaluating whether your operational controls prove you finish projects on time, on budget, and without drama.

The contractors who unlock the best bonding terms (lower premiums, faster approvals, higher capacity) aren't necessarily the ones with the most cash. They're the ones who demonstrate through documented systems and proven track records that they minimize surety risk. Here's how to build that story.

Understanding Contractor Surety Bonds: The Basics

A surety bond is a three-party performance guarantee connecting the contractor, the project owner, and the surety company. Unlike insurance, which protects you from losses, a bond protects the project owner from your failure to perform. If you default, the surety steps in to complete the work or compensate the owner, then comes after you to recover those costs.

Three bond types dominate construction bonding:

- Bid bonds guarantee you'll sign the contract if awarded the project

- Performance bonds guarantee project completion according to contract terms

- Payment bonds guarantee you'll pay subcontractors and suppliers

Most public work and increasingly private projects require all three, take out

Bond premiums typically range from 0.5% to 3% of contract value. That's a wide spread, and it exists because operational controls matter enormously to surety underwriters. A $5 million project might cost you $25,000 in premiums with strong controls and clean history, or $150,000 if your risk profile raises red flags. Multiply that across a year's worth of bonded work, and the financial impact of how sureties perceive your operations becomes impossible to ignore.

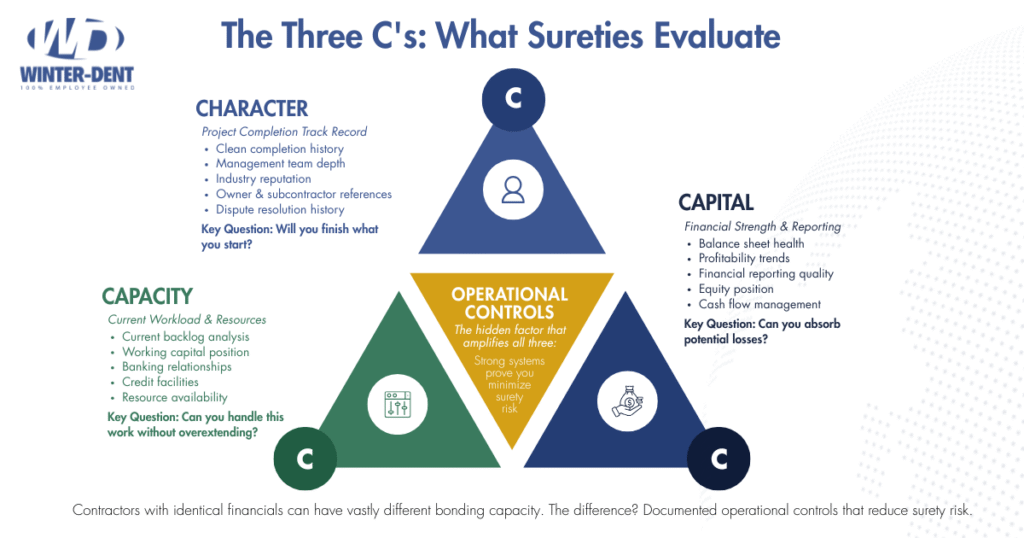

What Sureties Actually Evaluate: The Three C's

Surety underwriters have spent decades refining how they assess contractor risk, and it boils down to three core evaluations known as the Three C's: character, capacity, and capital. But what they're really asking underneath all the financial ratios and project lists is this: "How likely is it that we'll have to step in and finish a project for this contractor?"

Character

Character encompasses your project completion history, management experience, and industry reputation. Sureties want to see a clean track record of completing similar work on time and within budget. They'll dig into any past project problems, disputes with owners, or liens filed against you. They're also evaluating your management team's depth. If your business depends entirely on one key person, that's a risk factor. References from owners, architects, and even subcontractors carry weight here.

Capacity

Capacity measures your current workload and resources. Sureties analyze your current backlog, working capital position, banking relationships, and credit facilities. They're making sure you can handle the new bonded work without overextending. A contractor with $2 million in working capital might secure capacity for a single $10 million project but struggle to bond three simultaneous $5 million projects (even though the total contract value is lower) because the working capital has to support multiple concurrent projects, each with its own cash flow demands. Contractors rarely fail from lack of work; it’s usually the result of taking on more than they can handle.

Capital

Capital examines your financial strength through balance sheet health, profitability trends, and financial reporting quality. But here's where many contractors miss the opportunity: sureties don't just review your financials in isolation. They're assessing whether your operational controls reduce their risk of having to step in and complete a project. Strong job costing systems, timely financial reporting, and documented project management processes all signal to sureties that you catch problems early and fix them before they become crises.

Operational Controls That Unlock Construction Bonding Capacity

Here's the insight that changes everything: contractors with identical working capital can have vastly different bonding capacity. The difference isn't luck or relationships. It's operational controls that prove to sureties you complete projects on time and on budget.

Project Management Discipline

Sureties want evidence that you're managing projects proactively, not reactively:

- Real-time job costing that catches cost overruns lets you course-correct before losses become material

- Formal change order management processes ensure scope changes get documented and billed, not absorbed

- Subcontractor prequalification and oversight systems reduce the risk of sub defaults that cascade into your performance

- Quality control protocols with documented inspections show you're delivering to specification the first time

These aren't theoretical exercises. When a surety reviews your submission, they're looking for documentation: job cost reports, change order logs, subcontractor qualification criteria, inspection checklists. They want to see systems, not just spreadsheets.

Financial Reporting Excellence

- Monthly financials delivered within 20 days of month-end signal operational maturity

- Job-level profitability tracking that matches or exceeds contract estimates proves your estimating accuracy

- Cash flow forecasting that projects 90-120 days ahead shows you're managing working capital strategically, not scrambling for payroll

When sureties see consistent, timely financial reporting, they know you're running a business, not just managing one crisis after another.

Risk Management Integration

- Proactive communication with owners and subcontractors about schedule changes, potential delays, or budget pressures keeps small issues from becoming contractual disputes

- Contract review procedures that flag problematic terms before you bid reduce your exposure to unreasonable risk

These practices demonstrate the maturity that sureties reward with capacity increases and premium reductions.

Common Bonding Capacity Roadblocks and How to Fix Them

Even contractors with strong operations hit capacity walls. The good news? Most roadblocks have clear solutions if you plan ahead.

- Undercapitalization: You're generating strong revenue and profitability, but owner distributions or dividend payments have kept equity too low to support larger bonding capacity. Sureties multiply working capital by their risk tolerance to determine single project and aggregate limits. If your equity base is thin, even excellent operations can't overcome the math. The solution requires discipline: focus on retained earnings over 2-3 years, control distributions to build equity, and demonstrate consistent profitability that justifies surety confidence in your ability to absorb project losses without threatening other work.

- Rapid Growth: Your backlog is growing faster than your working capital can support it. This is a good problem to have, but it's still a problem if you can't bond the work you're winning. The solution starts with forecasting your bonding needs 12-24 months ahead, then working backward to determine how much equity you need to build through retained earnings. You may need to control your growth pace in the short term, turning down work that would exceed your current capacity while you build the balance sheet to support sustainable expansion.

- Poor Financial Reporting: Late or inconsistent financial statements signal weak operational controls to sureties, regardless of how strong your actual performance might be. Moving from compiled to reviewed or audited statements signals commitment to financial transparency, but the upgrade process typically takes 12-18 months as your CPA firm builds confidence in your internal controls. If you're planning to pursue bonding capacity growth, start the financial reporting upgrade now, not when you need capacity immediately.

- Past Project Problems: A default, significant loss, or contentious project dispute in your history raises red flags with every surety underwriter. You can't erase the past, but you can demonstrate you've learned from it. Document the corrective actions you implemented: upgraded estimating processes, enhanced project oversight, improved subcontractor prequalification, or strengthened project management staffing. Then prove those changes worked through 3-5 years of successful project completions. Sureties will give you a second chance, but they'll verify you've earned it.

Growing Your Bonding Capacity Over Time: A Realistic Timeline

Bonding capacity growth follows a fairly predictable path for contractors who execute well. Understanding the typical progression helps you plan realistically and avoid frustration when sureties don't immediately approve the limits you're hoping for.

Years 1-2: Building Your Track Record

Early-stage contractors typically start with project-specific bonds rather than an ongoing bonding program. You'll provide detailed financials and project plans for each bond request. Expect single project capacity of 5-10 times your working capital or net worth if you demonstrate strong operations and clean completion history. A contractor with $500,000 in working capital might bond individual projects up to $2.5-5 million, but aggregate capacity across all simultaneous bonded work will be limited.

Years 3-4: Transitioning to a Bonding Program

With consistent performance and growing equity, you can transition to a pre-approved bonding program where the surety commits to capacity limits without reviewing every individual project. Single project capacity often reaches 10-15 times working capital, and aggregate capacity expands to support multiple concurrent projects. That same contractor, now with $1.2 million in working capital and a proven track record, might secure a program with $12-18 million single project capacity and $30-40 million aggregate.

Years 5+: Maximum Capacity and Multiple Surety Relationships

Established contractors with strong financials, clean completion records, and documented operational systems can achieve single project capacity of 15-20+ times working capital. More importantly, you'll likely develop relationships with multiple sureties for backup capacity and market leverage. A contractor with $3 million in working capital might carry primary capacity of $50-60 million with one surety and backup capacity with another, providing flexibility when you're pursuing exceptionally large projects or maintaining multiple big jobs simultaneously.

What Accelerates This Timeline:

- Consistent profitability across every project in your backlog demonstrates estimating accuracy and operational efficiency.

- Clean completion history with owner references available upon request proves you deliver what you promise.

- Strong financial reporting systems that provide monthly statements within two weeks of month-end show operational maturity.

- Proactive communication with your surety partners about upcoming opportunities, potential challenges, or changes in your business builds trust.

- Documented operational controls that demonstrate how you manage projects, track costs, and mitigate risks give underwriters confidence in approving higher limits.

Preparing a Winning Surety Bond Submission

The quality of your surety bond submission directly impacts approval speed, capacity limits, and premium rates. Sureties receive countless submissions, and the ones that get approved quickly are the ones that answer all their questions upfront with well-organized documentation.

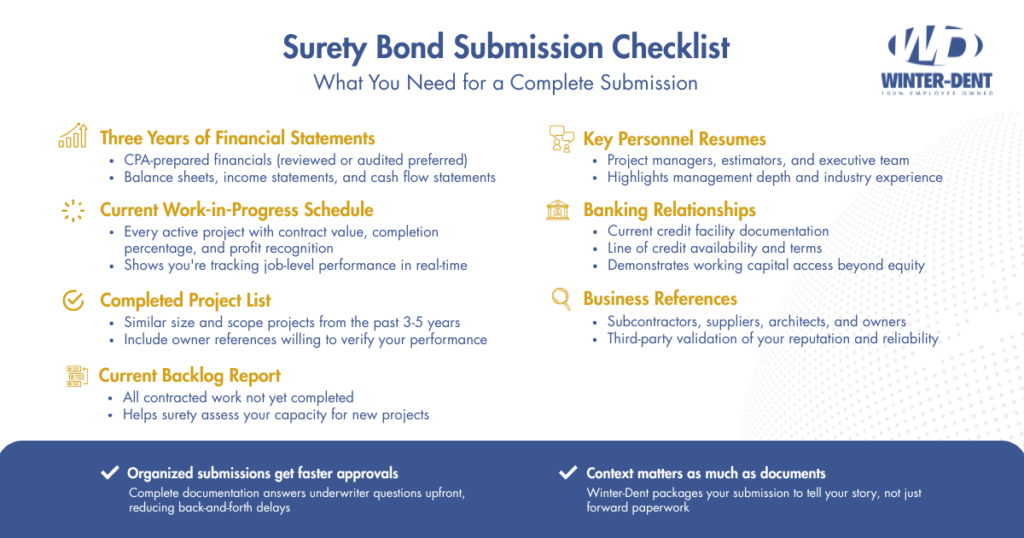

What Sureties Need to See:

- Three years of CPA-prepared financial statements, ideally reviewed or audited, demonstrate financial transparency and reporting quality.

- A current work-in-progress schedule showing every active project with original contract value, completed percentage, and profit recognition proves you're tracking job-level performance.

- A completed project list with references for similar size and scope work verifies your experience and gives the surety contacts to verify your reputation.

- Banking relationships and credit facility documentation show you have working capital access beyond just equity.

- Key personnel resumes establishing management depth and industry experience reduce concerns about key person dependency.

But here's what separates adequate submissions from compelling ones: context.

Raw financials don't tell your story. At Winter-Dent, we don't just forward your documents to a surety. We package submissions to tell your story by highlighting operational strengths, addressing any concerns proactively, and presenting you as a contractor sureties want to partner with long-term. That means explaining the "why" behind your numbers: why a particular year showed lower profitability, how you've strengthened operations since then, what systems you've implemented to ensure consistent performance going forward.

Winter-Dent's Prevent365 Approach to Surety Bond Programs

Most insurance brokers treat surety bonds as a transactional service: you submit your financials, they forward them to a surety, you get approved or declined. We see it differently.

Building sustainable bonding capacity requires preventing problems before they affect your surety relationship, containing issues when they inevitably arise, and positioning your risk profile strategically to negotiate the best possible terms.

Prevent

We help contractors build the operational controls and financial systems that sureties reward. That includes project management discipline with real-time job costing and change order tracking, safety programs that reduce incident frequency and severity, quality control systems that minimize rework and warranty claims, and financial reporting excellence that demonstrates operational maturity. When you're implementing these systems proactively (before you need bonding capacity) sureties see a contractor who understands risk management, not one who's scrambling to meet their requirements.

Contain

Project challenges happen to every contractor. What separates companies that maintain strong surety relationships from those who lose bonding capacity is how they respond. We coordinate response strategies to minimize financial impact and protect your bonding relationships through proactive communication. When a project hits trouble, your surety needs to hear about it from you first, with a clear plan for resolution. We help you develop that communication strategy and present it in a way that maintains surety confidence even during difficult situations.

Insure

We present your risk profile strategically to sureties, highlighting operational strengths and negotiating competitive terms based on your operational quality, not just your balance sheet. That means knowing which sureties specialize in your type of work, understanding how each underwriter evaluates risk, and positioning your submission to emphasize what makes you a low-risk partnership opportunity.

The Result

Contractors working with Winter-Dent typically achieve a clearer path to increased bonding capacity through documented operational improvements that sureties recognize and reward, faster bond approval and issuance, which are critical when you're working against tight bid deadlines, and stronger surety relationships that weather market cycles. When surety markets tighten and capacity becomes scarce, sureties protect relationships with contractors who've proven they're low-risk partners.

Get Your Complimentary Surety Analysis

Whether you're pursuing your first bonded project or looking to expand capacity to support larger work, the path forward starts with understanding where you stand today. Winter-Dent's complimentary Surety Analysis reviews your financials, operational controls, and project history to determine your current bonding capacity and creates a customized roadmap for growth.

We'll help you understand what sureties see when they evaluate your submission, identify operational improvements that will unlock higher capacity, develop a timeline for achieving your bonding goals, and position your risk profile to negotiate the most competitive terms available in the current market.

Because at the end of the day, bonding capacity isn't just about your balance sheet. It's about proving to sureties that you've built the operational controls that make you a contractor they want to partner with for the long term.

Frequently Asked Questions About Contractor Surety Bonds

How long does it take to get approved for a surety bond?

For contractors with an established bonding program, individual project bonds can be issued within 24-48 hours. First-time bond applicants should expect 1-4 weeks (depending on size of project) for the surety to review financials, complete underwriting, and establish initial capacity limits. The timeline depends heavily on how organized your submission is and whether you proactively address potential underwriting questions.

Do I need bonding capacity for every project I bid?

Not necessarily. Most public sector work and some larger private projects require bonds, but smaller private projects often don't. However, having bonding capacity opens doors to opportunities you'd otherwise have to pass on. Many contractors find that once they establish a bonding program, they naturally gravitate toward bonded work because it often involves better-capitalized owners and more clearly defined contract terms.

What's the difference between aggregate capacity and single project capacity?

Single project capacity is the largest individual project the surety will bond for you. Aggregate capacity is the total amount of bonded work you can have in progress simultaneously across all projects. For example, you might have $15 million single project capacity but only $40 million aggregate capacity. That means you could bond one $15 million project plus several smaller ones, but not three $15 million projects at the same time.

Can I get bonded if I've had project problems in the past?

Yes, but it requires demonstrating you've learned from those experiences and implemented corrective measures. Sureties understand that project challenges happen. What they want to see is 3-5 years of successful completions following the problem, documentation of the operational improvements you made, and transparency about what went wrong and how you fixed it. Trying to hide past issues always backfires during underwriting.

How much does it cost to maintain a bonding program?

Beyond the per-project bond premiums (typically 0.5% to 3% of contract value), there are no separate fees to maintain a bonding program with most sureties. The real cost is the operational investment: upgraded accounting systems, potentially moving to reviewed or audited financials, and implementing the project management controls that sureties expect. These investments pay dividends beyond just bonding, they make you a more profitable, better-run company overall.

What happens if a project goes badly and the surety has to step in?

If a surety has to complete a project or compensate the owner due to your default, they will pursue you for reimbursement. Unlike insurance, surety bonds are essentially credit instruments. The surety expects to be made whole for any losses. This is why sureties are so careful about underwriting, they're extending you credit based on their confidence you won't default. A surety claim can also make it extremely difficult to obtain bonding capacity in the future, which is why maintaining strong project controls and communication is critical.