Pop quiz: What's the single biggest insurance cost increase hitting businesses in 2026?

If you guessed cyber liability or workers' compensation, you'd be wrong. Commercial auto insurance premiums continue to surge at rates that make even the most seasoned CFOs wince. For fleet operators, the question isn't whether rates will increase, but how much and, more importantly, what you can actually do about it.

The hard market for commercial auto insurance isn't new. What makes 2026 different is the convergence of factors creating a perfect storm: nuclear verdicts are accelerating, carrier capacity continues shrinking, and driver quality issues compound the risk. Understanding these dynamics isn't just about budget planning. It's about survival in an industry where margins are tight, and one major accident can erase years of profits. More critically, the traditional approach of shopping for better rates has reached its limit. What's needed is a fundamental shift in how fleets approach risk itself.

The Numbers Behind the Crisis

Let's start with the premium increases that keep transportation executives up at night:

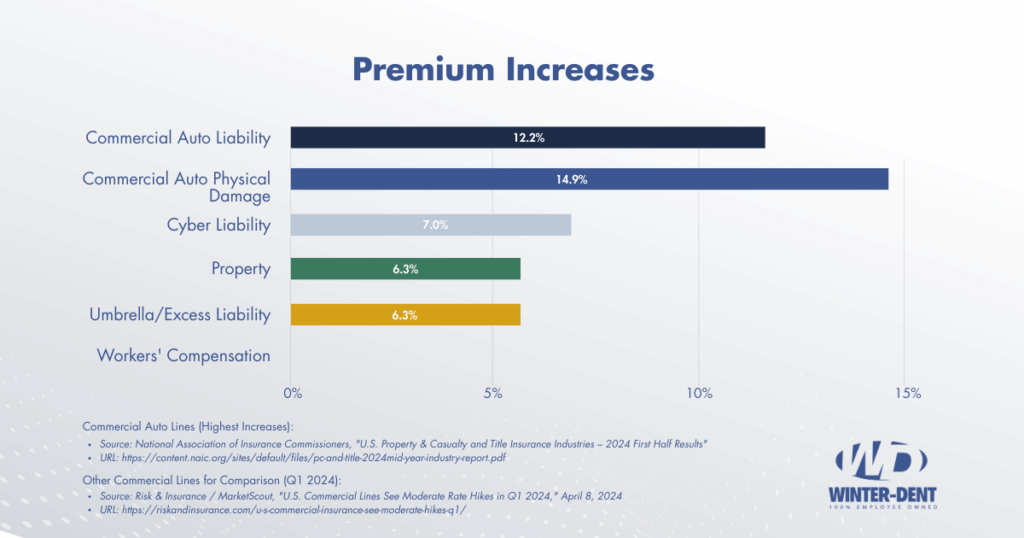

- Commercial auto liability premiums increased 12.2% in the first half of 20241

- Physical damage coverage jumped 14.9% in the same period, the highest percentage growth among all major commercial lines1

- Early 2025 data shows commercial auto leading all lines at 6.7% rate increases2

For a mid-sized fleet running 50 trucks, these aren't abstract percentages on a spreadsheet. They translate to six-figure premium increases over just two years, with no relief in sight.

But the raw numbers tell only part of the story. What makes the current environment particularly dangerous is the simultaneous reduction in carrier capacity. Major insurers have pulled back from the commercial auto space entirely, while others have dramatically narrowed their risk appetite. The result? What used to be a competitive market with multiple quotes has become a scramble to find any carrier willing to write coverage. Some fleets are discovering they're effectively uninsurable at any price.

Why Carriers Are Fleeing Commercial Auto

So what's driving this capacity crisis? The answer lies in courtrooms across the country. Nuclear verdicts (jury awards exceeding $10 million) have become alarmingly common in commercial auto cases. Consider these statistics:

- Between 2010 and 2018, average verdicts in truck crash cases surged 1,000%, from $2.3 million to $22.3 million3

- A recent U.S. Chamber of Commerce study found the mean award reached $27.5 million for cases between June 2020 and April 20234

- Settlements averaged $10.6 million during the same period

When a single claim can exceed an insurer's entire annual premium collection from a fleet, carriers naturally reassess their appetite for the business. Many have decided the risk simply isn't worth the potential exposure.

Compounding this is social inflation, a phenomenon distinct from economic inflation. Social inflation reflects changing cultural attitudes toward corporations, increasingly aggressive plaintiff attorney tactics, and the rise of litigation funding. Together, these factors have contributed to a $30 billion surge in commercial auto claim costs between 2012 and 2021.5 The practical impact? Even routine accidents now generate settlement demands that would have been reserved for catastrophic cases just five years ago.

Meanwhile, claims severity continues climbing across every category. Medical costs for treating accident injuries have surged. Total loss values for commercial vehicles have jumped as new truck prices reached record highs. Inflation has driven claim expenses $95 billion to $106 billion higher than they would have been over the past decade.10 For fleet operators, every accident now carries financial exposure that far exceeds historical norms.

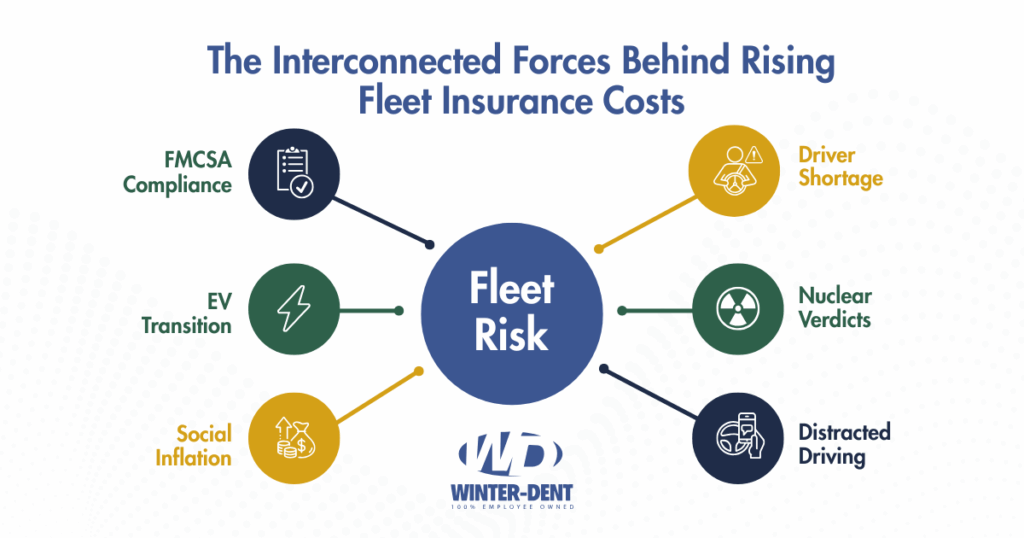

The Risk Factors You Can't Ignore

Understanding what's driving costs helps you focus prevention efforts where they'll have the most impact. Several interconnected factors are making fleets riskier and more expensive to insure:

The Driver Shortage Crisis

The driver shortage isn't just a capacity problem, it's a safety crisis. The American Trucking Associations estimates the industry was short roughly 60,000 drivers in 2024, with projections showing the shortage could reach 160,000 by 2030.6 This forces fleet operators into an impossible choice: run short-staffed (leading to tired drivers and rushed schedules) or hire less experienced drivers (leading to higher accident rates). Many businesses have lowered hiring standards just to fill seats, creating a dangerous cycle where inexperienced drivers contribute to rising loss ratios, which in turn drive up premiums for everyone.

The Distracted Driving Problem

Distracted driving has evolved beyond texting. Modern trucks come equipped with elaborate dashboard displays, multiple navigation systems, and electronic logging devices that constantly demand driver attention. While these technologies improve safety when used properly, they also create new distraction vectors. The National Safety Council estimates cell phone use while driving results in 1.6 million crashes annually. For commercial fleets, every distracted-driving incident becomes fodder for plaintiff attorneys arguing systemic negligence.

FMCSA Compliance and SMS Scores

Federal Motor Carrier Safety Administration (FMCSA) compliance issues carry weight far beyond regulatory fines. Your Safety Measurement System (SMS) scores directly impact insurability. Carriers with poor SMS scores in categories like Unsafe Driving or Hours of Service (HOS) Compliance can find themselves unable to secure coverage at any price. Even moderate scores translate to premium surcharges as insurers price for perceived risk.

The Electric Vehicle Transition

Electric vehicle adoption introduces new considerations. While EVs can reduce operating costs and meet sustainability goals, they present unfamiliar risks. Commercial fleet EV adoption is accelerating, with projections of over four million units by 2030.1 Battery fire risks, specialized repair requirements, and technician training gaps all contribute to uncertainty. Early EV adopters often face higher premiums simply because insurers lack sufficient loss data to price coverage accurately.

The Prevent365 Process: A Different Approach

Here's where most fleet operators miss the opportunity. They accept premium increases as inevitable, shop for slightly better rates, and hope for the best. That's not a strategy. That's surrender. The fleets maintaining sustainable insurance costs take a fundamentally different approach, viewing risk management as a core operational function rather than an insurance department problem.

At Winter-Dent, we call this the Prevent365 process. It's built on a simple but powerful principle: prevent what you can, contain what you can't prevent, and strategically insure what's left. Most brokers focus exclusively on that third step. We believe the first two steps determine whether your insurance program is financially viable. Here's how it works:

Prevent: Stopping Accidents Before They Happen

Prevention starts long before a truck leaves the yard. The first pillar of Prevent365 focuses on eliminating risk at its source through rigorous selection, training, and operational controls. Most fleets understand prevention in theory, but few implement it systematically enough to impact their loss ratios. The difference between mediocre and exceptional loss experience often comes down to consistency in executing preventive measures.

Driver Screening That Actually Works

Motor Vehicle Record (MVR) screening sounds basic, but the details matter enormously. Effective screening includes looking back at least three years, defining specific disqualifying events (any DUI/DWI, certain combinations of violations), and establishing a scoring system that weights recent violations more heavily. Most importantly, you need periodic checks on existing drivers, not just at hire. Fleets that only screen at initial employment can miss critical changes in driver behavior. Such an oversight could result in a six-figure claim and double-digit premium increases at renewal.

Training Beyond Compliance

Driver training programs often get short shrift in the rush to get trucks on the road. However, training quality directly correlates with accident frequency. Effective programs include vehicle-specific instruction, defensive driving techniques, adverse weather training, and ongoing coaching rather than one-time orientation. New drivers should spend significant time with experienced drivers before operating independently. Companies that treat training as a compliance exercise rather than a safety investment pay for it in their loss runs.

Telematics Done Right

Telematics and driver behavior monitoring have revolutionized fleet safety when implemented properly. Simply installing devices and collecting data accomplishes nothing. You need to actively use the data to coach drivers, recognize good performance, and address concerning patterns before they result in accidents. The most successful fleets focus on a handful of key metrics: harsh braking events, speeding incidents, seatbelt use, and following distance. They establish clear standards, provide regular feedback, and create positive incentives for improvement.

Maintenance as Prevention

Vehicle maintenance protocols might seem unrelated to auto liability, but breakdowns cause accidents. A tire blowout at highway speed can be catastrophic. Brake failure is self-explanatory. Preventive maintenance programs that address these issues before they cause roadside emergencies protect both your equipment investment and your liability exposure. Additionally, detailed maintenance records prove you took reasonable steps to ensure vehicle safety, documentation that becomes crucial when defending against negligence claims. Plaintiff attorneys will comb through your maintenance history looking for evidence of neglect. Don't give them ammunition.

Contain: Minimizing Damage When Incidents Occur

The second pillar of Prevent365 recognizes a fundamental truth: no matter how strong your prevention efforts, incidents will occur. The question is whether you're prepared to contain the damage. Containment isn't about denying responsibility or hiding from accountability. It's about responding to incidents in ways that protect your drivers, minimize injury and property damage, preserve evidence, and position you to defend claims effectively. This is where many fleets lose control of their costs.

The Dashcam Advantage

Dashcam programs deliver perhaps the highest return on investment of any containment technology. Forward-facing and driver-facing cameras serve multiple purposes: exonerating drivers in not-at-fault accidents, providing training opportunities by capturing near-misses, and modifying driver behavior through awareness of recording. The data is compelling. Studies show dash cams combined with driver coaching reduce safety-related events by 52%.7 Fleets adopting comprehensive AI safety solutions including dual-facing cameras, in-cab alerts, and AI coaching see approximately 75% decrease in crash rates over 30 months.7

The ROI on dashcams is both measurable and dramatic. Organizations using fleet telematics and video-based safety solutions realized an average 815% return on investment and reduced fleet-related operational costs by 6%.8 Consider a hypothetical mid-sized fleet that invests $150,000 in a full-fleet dashcam system.9 In year one, video evidence successfully defends against three major liability claims where the fleet would have otherwise settled or faced significant exposure. The camera footage provides indisputable evidence the drivers weren't at fault. In such scenarios, savings on just three claims could exceed $800,000. When you factor in the premium impact that would have resulted from those paid claims, the cameras could pay for themselves in less than three months. Forward-thinking fleets increasingly view dashcams not as a safety expense but as a profit center.

Post-Accident Protocols

Beyond technology, effective containment requires clear post-accident protocols. Drivers need to know exactly what to do immediately after an incident: who to contact, what information to collect, what to never say. Many claims that could have been defended successfully are lost because drivers made statements at the scene that were later used against them. Training drivers on proper post-accident procedures is as important as training them to avoid accidents.

Rapid Response Teams

For serious accidents, rapid response teams that can deploy to accident scenes make a significant difference in claim outcomes. These teams secure evidence, interview witnesses while memories are fresh, and ensure proper documentation before scenes are cleared. In cases involving serious injuries or fatalities, the first 24 hours often determine whether you'll face a reasonable settlement or a nuclear verdict. Having someone on-site who understands both legal and operational implications is invaluable.

Insure: Strategic Coverage for Residual Risk

The third pillar of Prevent365 addresses what remains after you've prevented what you can and contained what you couldn't prevent. This is where most brokers start and stop, but when it's built on a foundation of strong prevention and containment, your insurance program becomes significantly more effective and affordable. Strategic insurance design isn't about buying the cheapest coverage. It's about structuring programs that match your actual risk profile and reward your prevention efforts.

Higher Retention Strategies

Higher retentions make sense for fleets with strong safety programs and adequate cash flow. By taking on more risk through higher deductibles, you can potentially reduce premiums, depending on your loss history. The key is matching your retention level to your actual loss experience. If you're preventing most accidents through strong safety programs, you won't tap those higher deductibles frequently. This requires careful analysis of detailed loss history, realistic projections, and sufficient working capital to handle multiple deductible hits in a bad year.

Alternative Risk Financing

For larger fleets, captive insurance programs or large deductible arrangements offer even more control. These structures allow you to essentially insure yourself for smaller claims while maintaining catastrophic coverage for major accidents. Premium savings can be dramatic compared to traditional programs, depending on the fleet's size and loss experience, because you're eliminating the insurer's profit margin on frequency claims. The trade-off is taking on more risk and responsibility. Captive programs require sophisticated claims management, adequate capital reserves, and strong internal controls. They're not for everyone, but if your combined commercial auto and workers' comp spend exceeds $250,000 and you maintain solid loss control programs, they often represent the most cost-effective long-term solution.

Usage-Based Programs

Usage-based insurance programs tie premiums directly to actual miles driven, routes traveled, and driving behaviors. These programs benefit seasonal operations or fleets with highly variable utilization. If your trucks sit idle for significant periods, why pay annual premiums based on full-time use? Usage-based programs price for actual exposure while providing more accurate risk assessment.

Translating Safety into Premium Savings

The connection between safety investments and premium reductions often gets lost in renewal negotiations. Strong safety programs should translate to better pricing, but you need to document your efforts and present them effectively. This means tracking key safety metrics, calculating improvement percentages, and quantifying the impact on loss experience. When we present renewals for clients with strong Prevent365 processes in place, we can come armed with data and give underwriters the justification they need to offer better pricing.

Why Winter-Dent's Approach Works

Most insurance brokers approach commercial auto the same way: collect information, submit to carriers, present the best quote. That's not worthless, but it won't solve the fundamental cost problem. When every fleet faces the same hard market, simply shopping harder delivers diminishing returns. You're competing for limited capacity with the same loss profile as your competitors. Unless you change that loss profile, you're just rearranging deck chairs.

Winter-Dent takes a different approach because we're built differently. As an employee-owned company, our interests align with yours in ways traditional brokerages can't match. We don't maximize revenue by selling more coverage or placing you with whichever carrier pays the highest commission. We succeed when you control costs and avoid losses. That alignment changes everything about how we work with clients.

Our process includes:

- Comprehensive audits of your safety program, not just your insurance policy

- Analysis of hiring practices, training protocols, maintenance schedules, and telematics data

- Loss run analysis to identify patterns pointing to preventable accidents

- SMS score assessment with specific improvement recommendations

- Customized prevention measures tailored to your specific loss drivers

This diagnostic phase typically takes 60 days and involves interviews with drivers, safety managers, and operations leaders.

The goal? Understanding not just what's happening but why it's happening, so we can design interventions that actually work given your resources and constraints.

Additionally, those improvements translate directly to premium savings, better coverage terms, and sustainable long-term costs even as the broader market continues hardening. Consider the real-world impact: a fleet spending $500,000 annually on commercial auto insurance that achieves a 30% loss ratio improvement could potentially save $150,000 per year in premiums. Over five years, that's $750,000 in cost avoidance, before considering operational benefits like reduced downtime, lower workers' compensation costs, and improved customer service.

Taking Action in 2026

Let's be clear about what's ahead. Commercial auto insurance isn't getting cheaper in 2026. Nuclear verdicts aren't going away. Carrier capacity won't magically reappear. The driver shortage will continue. These realities aren't changing. The question is whether you'll adapt or simply accept escalating costs as the new normal.

The traditional playbook (shopping for better rates and hoping for market softening) is no longer viable. What's needed is a fundamental shift in how fleets approach risk. The fleets that will thrive are those recognizing insurance as the last step in risk management, not the first. They invest in prevention, measure results, and use those results to negotiate better insurance terms. They view safety not as a compliance obligation but as a competitive advantage.

If you're ready to stop accepting premium increases as inevitable and start taking control of your risk profile, Winter-Dent can help. Our Fleet Risk Assessment reviews your loss runs, evaluates your current safety programs, and identifies specific premium reduction opportunities. We examine your prevention efforts, containment capabilities, and insurance program design through the lens of the Prevent365 process.

The assessment typically takes 60 days and results in a detailed roadmap showing exactly where you're leaving money on the table and what specific steps will deliver the best return. Because we're employee-owned, we're focused on your long-term success, not short-term commissions. Our compensation aligns with your interests: we succeed when you achieve sustainable cost reduction and improved safety performance.

The cost of transportation risk is rising, but that doesn't mean your costs have to rise at the same rate. The difference comes down to whether you're willing to do the work most fleets won't. Prevention isn't glamorous. It requires consistent execution of fundamentals, accountability at every level, and saying no to marginal drivers even when you're desperate for capacity. But it's profitable. And in 2026's market, profit margins may well depend on it.

Sources

2. Risk & Insurance, "Commercial Insurance Rates Rise 3% on Average in Q1 2025," April 7, 2025

3. American Trucking Associations, "How Nuclear Verdicts are Strangling America's Trucking Industry"

6. American Trucking Associations, "ATA Chief Economist Pegs Driver Shortage at Historic High"

7. Samsara, "Capture ROI from Your Fleet Safety Program"

8. Pro-Vision Solutions, "Calculating the Real ROI of Fleet Dash Camera Systems," June 20, 2025

9. HD Fleet, "Fleet Dash Cams - What Every Fleet Manager Needs to Know," February 28, 202510. Insurance Information Institute, "U.S. Auto Insurer Claim Payouts Soar Due to Increasing Inflation," September 28, 2023