If you're responsible for protecting your organization (whether you're in the C-suite, running safety operations, or leading HR), you've probably noticed the playbook that worked five years ago doesn't work anymore. Cyber threats aren't just IT problems. Weather events aren't just facilities issues. Workforce challenges aren't just hiring headaches. They're all enterprise risks that show up on your P&L, in your incident reports, and in increasingly expensive insurance renewals.

At Winter-Dent, we've identified six trends reshaping organizational risk in 2026. More importantly, we've identified what you can actually do about them before they show up as losses.

Here's where we part ways with most brokers. When an organization calls asking about coverage, many brokers immediately start talking policy limits and premiums. We start with a different question: What could you prevent from happening in the first place?

That's the heart of our Prevent365 process: prevent what you can, contain what you can't prevent, and insure what's left. It requires coordination across functions, but by the time we're talking about policy terms, your entire organization has already reduced its risk profile.

Let's dig into what's coming in 2026.

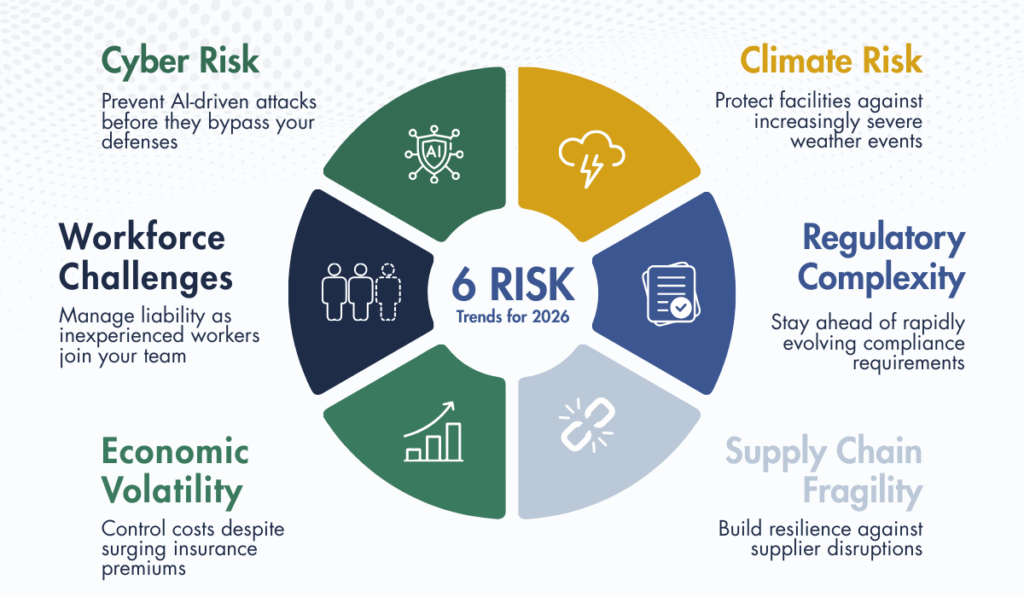

1. Cyber Risk Evolution: When Artificial Intelligence Becomes a Weapon

Cybersecurity has entered a new era where threats don't look like the phishing campaigns IT teams trained everyone to spot. Artificial intelligence has changed the rules, enabling attack methods that were purely theoretical just a few years ago.

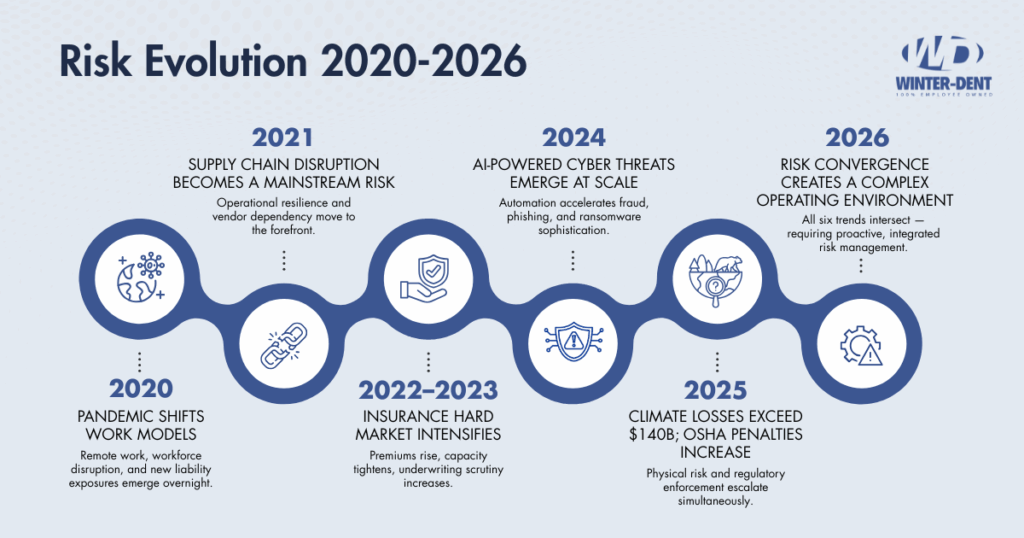

Consider what happened to Arup, a global engineering firm with sophisticated security protocols. In early 2024, the company lost $25 million to a deepfake scam.¹ A finance employee received a video conference call where they saw and heard what appeared to be their CFO and several colleagues. Every participant except the victim was an AI-generated deepfake. The employee transferred $25 million before discovering the fraud.

This isn't isolated. The technology to create convincing deepfakes is increasingly accessible. Traditional approval workflows that rely on recognizing voices or faces no longer provide adequate protection. Executive communications (earnings calls, conference presentations) are creating the training data criminals use to impersonate leadership.

Cyber incidents increasingly affect physical operations. Ransomware can shut down production lines and lock access to safety systems. Your remote workforce is your cyber perimeter now, with every home office a potential entry point. And when a breach occurs, managing crisis communications and workforce notifications becomes critical.

Supply chain cyber attacks have become one of the fastest-growing threat vectors. Between 2021 and 2023, supply chain attacks increased by 431%.² When a managed IT services provider suffers a breach, dozens or hundreds of clients become vulnerable.

The Prevent365 Approach to Cyber Risk

Prevent: Implement AI-powered threat detection and multi-factor authentication across all systems. Conduct security awareness training addressing deepfakes and emerging threats. Include vendor risk management with security audits of critical suppliers.

Contain: Develop incident response plans that treat cyber events like fires. Segment your network so breaches don't compromise everything. Establish verification protocols for unusual financial requests using separate communication channels.

Insure: Cyber insurance is essential, but insurers increasingly require specific security controls before issuing policies. Review limits annually because incident costs have increased dramatically.

2. Climate-Related Property Risks: The New Normal Isn't Normal

Insurance actuaries have built their pricing models on the assumption that history predicts the future. But climate patterns are shifting in ways that render decades of actuarial data less useful. Events that models once categorized as "100-year storms" now occur multiple times per decade.

In 2024, global insured losses from natural disasters reached $140 billion.³ The insurance market has responded with higher premiums, reduced coverage, and in some cases, complete withdrawal from high-risk markets.

The challenge extends beyond obvious high-risk zones. Manufacturing facilities face equipment failures during unprecedented heat waves. Distribution centers with no flood history experience their first flood event. Cold snaps cause pipe bursts in buildings with previously adequate insulation.

The Prevent365 Approach to Climate Risk

Prevent: Conduct climate vulnerability assessments using forward-looking models. Upgrade building systems proactively with improved drainage, reinforced roofing, and backup power.

Contain: Develop scenario-specific business continuity plans. Identify alternative suppliers in different geographic areas so a single weather event can't halt operations.

Insure: Review coverage limits annually because replacement costs have increased dramatically. Understand your policy's business interruption coverage thoroughly.

3. Workforce Challenges: The Talent Crisis Meets Liability Exposure

The talent shortage headlines focus on recruitment costs, but workforce problems are creating liability exposures across every function. Organizations are hiring people with less experience than they'd prefer, and that shows up in incident reports.

Inexperienced workers have higher injury rates across all industries. Remote work has created legal ambiguity around workers' compensation, cybersecurity liability, and employment practices. Worker misclassification (independent contractor versus employee) has never been riskier from a compliance standpoint.

The financial impact extends beyond recruitment expenses. Workers' compensation claims from inexperienced workers cost more. Employment practices liability claims from misclassification can be substantial. And talent shortages in critical roles create operational risks.

The Prevent365 Approach to Workforce Risk

Prevent: Invest in comprehensive onboarding and ongoing training, especially for safety-critical positions. Develop clear remote work policies addressing cybersecurity and work-hour boundaries. Conduct regular classification audits.

Contain: Implement near-miss reporting systems. Establish clear escalation procedures for employment disputes. Monitor leading indicators like overtime hours that predict incidents.

Insure: Review workers' compensation, employment practices liability, and general liability policies with an agent who understands remote work exposures. Ask about coverage for states where you have remote employees but no physical presence.

4. Regulatory Complexity: Compliance as a Moving Target

Regulatory complexity has reached a point where even dedicated compliance professionals struggle to keep up. And the penalties for getting it wrong have gotten more expensive.

Regulatory penalties hit bottom lines directly. OSHA (Occupational Safety and Health Administration) violations can shut down operations. CMMC (Cybersecurity Maturity Model Certification) non-compliance can disqualify you from contracts. State-level employment law violations can trigger class action lawsuits.

OSHA enforcement has intensified significantly. Maximum penalties for serious violations increased to $16,550 per violation in 2025, while willful violations now carry penalties up to $165,514.⁴ Some 2025 penalties exceeded $4 million for facilities with multiple repeat violations.⁵

Employment law varies dramatically by state. What's compliant in Texas may violate California law. Cybersecurity regulations like CMMC have moved from proposed frameworks to strict requirements, and healthcare organizations navigate HIPAA (Health Insurance Portability and Accountability Act) enforcement with higher penalties while financial services firms implement evolving SEC (Securities and Exchange Commission) cybersecurity disclosure requirements.

The Prevent365 Approach to Regulatory Risk

Prevent: Build regulatory monitoring into operations with clear ownership assignments. For multi-jurisdictional operations, consider compliance management software. Conduct regular internal audits because finding problems yourself is always better than having regulators find them.

Contain: When you discover potential violations internally, address them immediately and document corrective actions. Develop clear procedures for regulatory inspections.

Insure: EPLI (Employment Practices Liability Insurance) and D&O (Directors and Officers) insurance increasingly cover certain regulatory penalties and defense costs. Review policies to ensure coverage addresses your regulatory exposure profile.

5. Economic Volatility: The Hidden Cost of Uncertainty

Insurance renewal premiums are jumping significantly across most industries. Commercial insurance rates rose by an average of 3.75% in 2024, while homeowners insurance increased 24% over the past three years.⁸ It's not your loss history driving this. Something fundamental is happening in the insurance market.

Claims costs have increased substantially. Construction costs have risen more than 40% in recent years, with labor costs up over 30%.⁶ Between October 2014 and October 2024, residential reconstruction costs rose by 63.7%.⁷ The dwelling coverage limit that properly insured your building three years ago may now leave you substantially underinsured.

The Prevent365 Approach to Economic Risk

Prevent: Maintain core risk management investments regardless of economic pressure. Organizations that defer maintenance often face much larger losses when systems fail.

Contain: Build flexibility into your insurance program. Higher deductibles can significantly reduce premiums if you have financial capacity to retain more risk.

Insure: Review coverage limits annually and adjust based on updated replacement cost estimates. Broker relationships become critical when capacity is limited and rates are increasing.

6. Supply Chain Fragility: When "Just-in-Time" Becomes "Too Late"

Supply chain optimization strategies (lean inventory, just-in-time delivery, single-source relationships) work brilliantly in stable conditions. The problem is that stability has become the exception.

Recent years exposed how fragile optimized supply chains can be. Political instability affects production and shipping. Trade disputes create sudden barriers. Natural disasters damage facilities. Any of these can cascade through supply chains, affecting organizations with no direct exposure to the initial disruption.

Consider the ripple effects: A typhoon damages semiconductor manufacturing in Taiwan, which affects electronics manufacturers in California, which impacts automotive plants in Michigan. The connection between initial event and final impact isn't always obvious, but it's real.

Just-in-time models compound these challenges. Lean inventory works when deliveries are predictable. When they're not, lack of buffer inventory means any disruption immediately affects operations.

The Prevent365 Approach to Supply Chain Risk

Prevent: Map your supply chain at least three tiers deep for critical items. Build relationships with alternative suppliers before you need them. Consider geographic diversification as risk management.

Contain: Develop tiered response plans for different disruption scenarios. Identify which inventory items warrant larger safety stocks based on replacement difficulty.

Insure: Contingent business interruption insurance covers losses when suppliers cannot operate. Supply chain insurance can cover costs for finding alternative suppliers and expedited shipping.

Taking Action: From Awareness to Prevention

We just laid out six major risk trends reshaping organizational protection. The organizations that thrive in 2026 won't be the ones with the most insurance. They'll be the ones who prevented losses from happening in the first place.

That's what our Prevent365 process is about: prevent what you can, contain what you can't prevent, and insure what's left.

Prevent is about investing in the controls and systems that stop incidents before they happen. Better building systems. Security controls that stop breaches. Training that keeps people safe. Yes, this costs money upfront, but it's almost always cheaper than paying for the loss (and dealing with the premium increases that follow).

Contain is about making sure that when something goes wrong (because it will), it doesn't become catastrophic. Good emergency response plans. Business continuity arrangements that you've tested. Backup systems that work when you need them.

Insure is where insurance comes in as the financial backstop for the scenarios that could threaten your survival. But by the time you're buying that insurance, you've already reduced your risk profile through Prevent365. You're a better risk. And better risks get better terms.

Let's Talk About Your 2026 Risk Program

Winter-Dent can evaluate where your current program stands against what's coming in 2026, identify the gaps that matter most, and help you build a plan that addresses them using the Prevent365 process.

We're employee-owned, which means our interests are aligned with yours in a way that's different from how most brokerages operate. We succeed when you successfully manage risk (not just when we sell you a policy).

Contact Winter-Dent to schedule your 2026 risk assessment.

Sources:

- CNN Business. "Finance worker pays out $25 million after video call with deepfake 'chief financial officer'." February 4, 2024. https://www.cnn.com/2024/02/04/asia/deepfake-cfo-scam-hong-kong-intl-hnk

- Foley & Lardner LLP. "Combatting Supply Chain Cyber Threats: Safeguarding Data and Protecting Digital Supply Chains in a Rapidly Evolving Cyber Landscape." October 29, 2025. https://www.foley.com/insights/publications/2025/10/combatting-supply-chain-cyber-threats-and-protecting-digital-supply-chains/

- Insurance Journal. "Insured Losses From Natural Disasters Hit $140B as Climate Change 'Shows Its Claws'." January 9, 2025. https://www.insurancejournal.com/news/international/2025/01/09/807524.htm

- U.S. Department of Labor. "US Department of Labor announces adjusted OSHA civil penalty amounts for 2025." January 15, 2025. https://www.osha.gov/news/newsreleases/osha-trade-release/20250114

- ISHN. "10 of the Biggest OSHA Fines of 2025." August 21, 2025. https://www.ishn.com/articles/114885-10-of-the-biggest-osha-fines-of-2025

- Bankrate. "Average homeowners insurance cost in December 2025." https://www.bankrate.com/insurance/homeowners-insurance/homeowners-insurance-cost/#cost-by-state

- Insurance Journal. "Rebuilding Costs Rose More Than 60% in the Last Decade: Verisk." February 21, 2025. https://www.insurancejournal.com/news/national/2025/02/21/812689.htm

- Insurance Business America. "US insurance rates reflect mixed trends in 2024." January 7, 2025. https://www.insurancebusinessmag.com/us/news/breaking-news/us-insurance-rates-reflect-mixed-trends-in-2024-519535.aspx; Consumer Federation of America. "New Report Finds American Homeowners Faced 24% Increase in Homeowners Insurance Premiums Over the Past Three Years." April 2, 2025. https://consumerfed.org/press_release/new-report-finds-american-homeowners-faced-24-increase-in-homeowners-insurance-premiums-over-the-past-three-years/

This article is for informational purposes only and does not constitute professional advice. Organizations should consult with qualified risk management and insurance professionals to address their specific circumstances.