A strategic guide for business owners, CFOs, HR leaders, and operations executives evaluating captive insurance structures.

Captive insurance is gaining real traction among mid-size and larger organizations as a tool for controlling insurance costs, building reserves, and reducing dependence on the commercial market.

For many companies, the first conversation about captives begins with a simple question: Should we place workers' compensation into a captive?

That question is reasonable, but it may also be incomplete.

In many cases, the one of the most financially effective captive structures is not a single-line program at all, but a multi-line captive that integrates workers' compensation, general liability, and commercial auto into a single risk vehicle. In many cases, workers’ compensation serves as the foundational line before general liability and commercial auto are added to the captive.

The real question leaders should ask is not whether to consider a captive, but whether starting with only one coverage line (workers’ compensation) leaves meaningful financial advantages on the table.

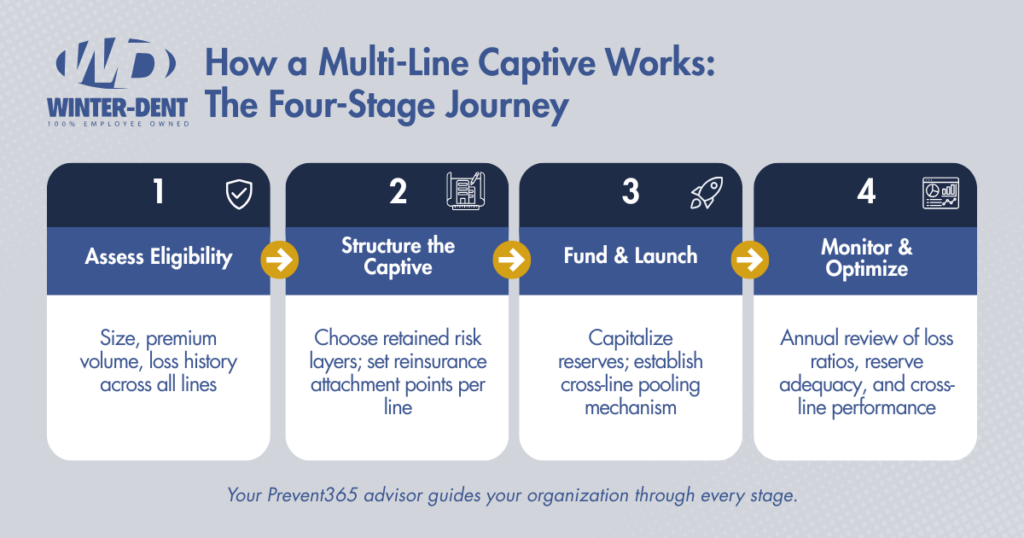

This article walks through the essential questions business leaders are asking about multi-line captives: how they work, whether they are more stable than single-line structures, how risk is structured across coverage lines, and what kind of organization is genuinely positioned to benefit.

Why Is Everyone Talking About Captives Right Now?

Over the past several years, many business leaders have started looking more seriously at captive insurance structures. The shift is not happening by accident. Several forces in the commercial insurance market are pushing organizations to reevaluate how they finance risk.

First, the traditional insurance market has become increasingly volatile. Premium swings, higher deductibles, and tighter underwriting have made long-term cost planning more difficult for many organizations.

Second, claims severity in several lines, particularly commercial auto and general liability, has increased across the industry. Insurers are responding by raising rates and reducing capacity in certain sectors.

Third, many companies with strong safety cultures are realizing that their loss performance is often better than the market average. In the traditional insurance model, those organizations effectively subsidize weaker performers in the same risk pool.

Captives change that equation. Instead of transferring all premium to a commercial carrier, organizations can retain a portion of their own risk, build reserves, and potentially capture underwriting profit when losses are lower than expected.

For companies that already manage risk proactively, captives transform insurance from a recurring expense into a strategic financial tool.

What Is a Multi-Line Captive?

A captive is an insurance company you own or co-own with other businesses, specifically created to insure your own risks. Rather than paying premiums to a commercial carrier and watching that money leave your balance sheet permanently, your premiums flow into the captive. When losses occur, the captive pays them. When losses are lower than expected, the surplus stays with you.

A single-line captive covers one type of risk, most commonly workers' compensation. A multi-line captive expands that structure to cover multiple types of risk simultaneously, typically two or more of the following:

- Workers' compensation

- General liability

- Commercial auto

The core difference is not just coverage breadth. It is how risk is structured, allocated, and capitalized across those lines. When multiple lines are placed within a single captive vehicle, each line remains separately evaluated and managed, even though all lines sit within the same overall structure.

Is It Better to Start with Workers' Compensation Only?

Workers' compensation is the most common entry point into captive insurance, and for good reason. Claims are frequent and relatively predictable, which makes actuarial modeling more reliable. Loss data is usually strong and well-documented. And regulators across most states have clear frameworks for workers' comp captives, which simplifies the approval process.

Starting with workers' compensation also gives your organization time to build familiarity with how a captive operates before adding complexity. You learn how to manage reserves, work with a captive manager, interpret loss reports, and engage with your reinsurance structure.

That said, starting single-line is not always the most financially efficient choice. If your organization already has meaningful premium volume across general liability and commercial auto, and you have a clean loss history across those lines, launching multi-line from the outset can generate greater reserve accumulation and better risk distribution from day one.

The right answer depends on your size, your loss data quality, and whether your organization has the operational infrastructure to manage a more complex structure at launch.

When Starting Single-Line Makes Sense

- You have 50 to 99 employees and are testing the model

- Workers' comp is your dominant premium line

- Loss data for GL and auto is inconsistent or thin

- Your team wants to build captive management experience before expanding

When Launching Multi-Line May Be Stronger

- You have 50 or more employees with significant premium across multiple lines

- Loss history across WC, GL, and auto is documented and stable

- Your combined annual premium is $250,000 or more

- You have strong risk management infrastructure already in place

Does Combining Workers' Comp, General Liability, and Commercial Auto Improve Financial Stability?

In most well-structured cases, yes. Here is why.

Each coverage line follows its own loss pattern and claim cycle. Workers' compensation claims tend to be frequent and moderate in severity, with predictable tails. General liability claims are often lower frequency but can carry significant severity. Commercial auto sits somewhere in between, with seasonal and geographic variability influencing outcomes.

When those three patterns run through separate commercial policies, your organization bears the full volatility of each independently. A bad year in workers' comp hits your mod, increases your renewal premium, and does nothing to offset a clean year in auto.

In a non-pooled multi-line captive, each line of coverage is structured and evaluated independently. Workers' compensation, general liability, and commercial auto each maintain their own reserves, reinsurance, and performance tracking.

While this structure does not allow one line to directly offset losses in another, it still improves overall financial visibility and control. Leadership gains a clearer understanding of how each risk category performs, which enables more targeted operational improvements and more precise risk management investment over time.

The result is not cross-line smoothing, but better-informed decision-making and stronger discipline across all lines of coverage.

How Does Cross-Line Pooling Work?

Cross-line pooling is the mechanism that makes multi-line captives more financially resilient than single-line structures.

In a traditional captive, reserves are allocated separately to each line of coverage. Workers' comp reserves fund workers' comp claims. GL reserves fund GL claims. If workers' comp performs exceptionally well and builds surplus, that surplus is typically held within that program and cannot be deployed against a GL claim in the same period.

In a multi-line structure with cross-line pooling, reserves are held in a shared pool that can respond to losses across any covered line. The captive holds a combined reserve base sized to the aggregate risk of all lines, not the sum of the maximum losses in each line independently.

For example, if workers' compensation, general liability, and commercial auto were each modeled separately, the combined capital requirement might total $3 million.

In a multi-line captive, actuaries model the probability that all three lines experience their worst year simultaneously, which is statistically unlikely. Because of that diversification, the required capital might be closer to $2 million rather than $3 million.

That is the logic behind pooled multi-line structures. However, not all multi-line captives are built this way. In a non-pooled structure, capital is allocated to each line independently based on its own risk profile. This typically results in a higher total capital requirement compared to a pooled model, because diversification credits are not applied across lines.

While this approach is more conservative, it provides a clearer and more transparent view of risk exposure within each coverage line.

How Does a Multi-Line Captive Work Without Cross-Line Pooling?

Not all multi-line captives use cross-line pooling. In many structures, each coverage line is intentionally kept financially independent, even though they operate within the same captive entity.

In a non-pooled multi-line captive, reserves are allocated and maintained separately for each line of coverage. Workers' compensation reserves fund workers' compensation claims. General liability reserves fund general liability claims. Commercial auto reserves fund auto claims. Surplus generated in one line is not used to offset losses in another.

This structure is often preferred by organizations that want greater transparency and control over each individual risk category.

For example, if workers' compensation performs well and generates surplus, that surplus remains within the workers' compensation program. If commercial auto experiences a higher-than-expected loss year, it draws only from its own allocated reserves and reinsurance structure, without relying on other lines for support.

From a capital standpoint, each line is modeled independently. Actuarial analysis determines the required reserves and capital based on the risk profile of that specific line, without applying diversification credits across lines. As a result, the total capital requirement is typically higher than in a pooled structure, but it provides a clearer, more conservative view of risk.

Reinsurance is also structured on a per-line basis. Each coverage line has its own attachment point, retention level, and excess coverage. This approach simplifies the reinsurance design and ensures that performance is evaluated independently across all lines.

Why would an organization choose this approach?

A non-pooled multi-line captive may make sense when:

- Leadership wants clear visibility into the performance of each line of coverage

- Loss history varies significantly between lines

- The organization is newer to captives and prefers a more controlled structure

- There is a desire to phase into a more integrated model over time

While this structure does not provide the same capital efficiency or cross-line risk smoothing as a pooled model, it still offers meaningful advantages over the traditional insurance market. Organizations retain underwriting profit within each line, gain greater control over claims and risk management, and build reserves that remain on their balance sheet.

Over time, some organizations choose to evolve from a non-pooled structure into a pooled model as their data matures and their confidence in managing multi-line risk increases.

Can Stronger Performance in One Line Offset Volatility in Another?

This is one of the most common questions business leaders ask when evaluating multi-line captives.

Consider a company with a strong workers' compensation program. Their investment in safety, return-to-work protocols, and claims management produces a loss ratio of 45% against their WC premium. In the same year, commercial auto has a rougher stretch due to fuel costs and fleet utilization changes, producing a loss ratio of 80%.

In a non-pooled multi-line captive, the answer is generally no.

Each line of coverage operates with its own reserves and financial structure, meaning strong performance in one line does not directly offset losses in another. Workers' compensation surplus remains within that program, while commercial auto or general liability must stand on their own results.

However, this separation can be a strategic advantage. It creates clear accountability by line of coverage, allowing leadership to identify exactly where performance is strong and where improvement is needed. Over time, that visibility can drive more effective risk management decisions than a fully blended structure.

The practical implication: Organizations that invest in risk reduction across all lines, not just workers' comp, can improve performance across the captive as a whole. Even in a non-pooled structure, stronger discipline across each line can strengthen the organization’s long-term overall results.

How Does Reinsurance Layer Across Multiple Lines?

Every captive retains some risk and transfers the rest. The portion transferred goes to a reinsurer, which steps in when losses exceed a defined threshold. This threshold is called the attachment point, and it determines how much your captive absorbs before the reinsurer pays.

In a single-line captive, reinsurance is structured specifically for that one line. Each claim above the per-occurrence or aggregate retention triggers the reinsurer.

In non-pooled multi-line captives, reinsurance is most commonly structured on a per-line basis, with each coverage line maintaining its own attachment point and excess coverage.

In a multi-line captive, reinsurance can be structured in several ways:

- Per-line reinsurance: Each coverage line has its own attachment point and reinsurance layer. This is often the clearest and most conservative approach, though it does not capture the same diversification benefits as pooled structures.

- Aggregate stop-loss reinsurance: The reinsurance attaches based on total losses across all lines combined. This allows the captive to retain more risk at a lower cost because the aggregate threshold accounts for diversification.

- Blended excess layers: Some captive structures layer reinsurance across the entire multi-line book, pricing the protection based on the correlation between lines rather than worst-case in each.

The right reinsurance structure depends on your risk tolerance, cash flow, and how correlated your loss patterns are across lines. An experienced captive advisor should model multiple scenarios before recommending which approach fits your organization.

Single-Line vs. Multi-Line Captive: At a Glance

| Factor | Single-Line Captive | Multi-Line Captive |

| Risk diversification | None — single exposure pool | Operational diversification, but financial results remain separate by line |

| Financial stability | Volatile; one bad claim year hurts badly | More controlled; each line evaluated independently |

| Capital efficiency | Reserves tied to one line only | Capital allocated per line; more conservative structure |

| Reinsurance cost | Higher per-line pricing | Per-line structured; cost varies based on retained risk and structure |

| Admin complexity | Lower — one program to manage | Higher — requires stronger infrastructure |

| Best suited for | 50-99 employees, testing the model | 100+ employees, stable multi-line loss history |

| Upside potential | Moderate | Strong within each line; less dependent on cross-line performance |

| Strategic control over insurance program | Limited | High |

Does Adding More Lines Increase Downside Risk?

This is a fair concern and deserves a direct answer.

Adding more lines does increase the total amount of risk being retained. However, in a non-pooled structure, that risk is segmented by coverage line rather than blended together.

This means each line must be properly capitalized and managed on its own merits. The benefit is greater clarity and control. The tradeoff is that organizations do not benefit from cross-line smoothing and must ensure that each program is financially sound independently.

Rather than behaving like a fully diversified portfolio, a non-pooled multi-line captive functions more like a set of parallel programs operating under a single structure. Each line contributes to the overall strategy, but performance is measured and sustained independently.

That said, the downside risk does increase meaningfully when:

- Loss data across the new lines is thin or inconsistent

- The organization's risk management discipline does not extend to the added lines

- The captive is undercapitalized relative to the expanded retained risk

- Reinsurance is improperly structured for the multi-line exposure

Proper feasibility analysis, actuarial modeling, and an ongoing advisory relationship mitigate these risks significantly. The question is not whether multi-line captives carry risk. They do. The question is whether that risk is well-understood, properly structured, and actively managed.

What Type of Organization Is Best Suited for a Multi-Line Structure?

A multi-line captive is not the right structure for every business. But for organizations that meet the qualifying criteria, it can be one of the most financially effective insurance strategies available.

The following profile describes organizations most likely to benefit:

- 50 or more employees with consistent headcount and operations

- Businesses spending $100,000+ annually on workers' comp premiums with a combined workers' comp, auto, and general liability minimum of $250,000

- At least three years of documented, stable loss history across workers' comp, GL, and/or auto

- A formal risk management function, even if it is a single dedicated person

- Leadership that views insurance as a financial strategy, not just a compliance requirement

- Ability to capitalize the captive and maintain reserve funding discipline

Organizations That See the Greatest Captive Returns

- Those with strong safety culture that produces consistently below-average loss ratios

- Companies with centralized operations that allow for standardized risk controls across locations

- Businesses with predictable growth trajectories, which allow accurate premium and loss modeling

- Organizations with proactive claims management programs, especially return-to-work for WC

Industries Where Multi-Line Captives Work Well

While captive insurance can be structured for many types of businesses, multi-line captives tend to work best in industries where organizations have meaningful exposure across several coverage lines, particularly workers' compensation, general liability, and commercial auto.

Industries that frequently benefit from multi-line captive structures include:

Manufacturing

Manufacturers often carry significant workers' compensation exposure alongside product liability and general premises liability risks. When combined with fleet operations for distribution, these organizations frequently have premium volume across all three lines.

Construction and Contracting

Construction firms typically face high workers' compensation exposure, along with general liability risks tied to project work and subcontractor relationships. Many also operate sizable vehicle fleets, making commercial auto another major line.

Distribution and Logistics

Companies involved in warehousing, trucking, or regional distribution often carry substantial commercial auto exposure alongside workers' compensation and liability coverage, making them strong candidates for multi-line structures.

Healthcare and Senior Care Systems

Healthcare organizations frequently have large workers' compensation programs along with professional liability and general liability exposures. In some structures, these lines can be incorporated into a broader captive strategy.

Multi-Location Service Businesses

Businesses operating across multiple locations, such as facility services, hospitality groups, or regional service providers, often generate stable loss data across several lines and may benefit from consolidating those risks into a captive structure.

The common thread across these industries is not simply size, but predictable operations and the ability to actively manage risk across multiple lines of coverage.

Ideal Candidate Profile: Are You Ready for a Multi-Line Captive?

Use this checklist to assess your organization's readiness. A strong multi-line candidate checks most of the solid boxes below, and has a clear plan to address the others.

| Qualifying Factor | What to Look For |

| Employee Count | Typically 50 or more employees across covered lines |

| Annual Premium | Combined premium of $250,000 or more across workers' comp, GL, and auto |

| Loss History | At least 3 years of stable, predictable loss data across multiple lines |

| Claims Discipline | Formal claims management process with documented return-to-work or incident response programs |

| Risk Culture | Leadership commitment to proactive risk management, not just compliance |

| Financial Reserves | Ability to fund initial capital requirements — typically 25-50% of retained risk |

| Multi-Line Exposure | Active exposure in at least two of the three lines: workers' comp, general liability, commercial auto |

| Advisor Relationship | An advisory broker who can structure, benchmark, and monitor captive performance annually |

The Prevent365 Perspective

At Winter-Dent, captive evaluation is not treated as a product recommendation. It is part of the Prevent365 risk advisory process, where we analyze how operational risk performance, insurance structure, and capital strategy interact over time.

A multi-line captive, structured correctly and monitored annually, can fundamentally change your relationship with risk. Instead of paying premiums into a market that profits from your losses, you build reserves that belong to you. Instead of absorbing the volatility of each line independently, you gain visibility and control across multiple lines of risk. And instead of renewing the same program every year and hoping the market cooperates, you gain measurable control over your long-term cost trajectory.

That outcome does not happen because you signed up for a captive. It happens because your organization makes a genuine commitment to understanding and reducing risk across every line of coverage. That is what Prevent365 is built to support.

*Important Note: This scenario is illustrative only and does not represent guaranteed results. Actual captive performance depends on many variables, including loss history, premium volume, industry risk characteristics, actuarial assumptions, and reinsurance structure. Organizations considering a captive should conduct a formal feasibility study before making any decisions.

This article is for informational purposes only and does not constitute legal, tax, or insurance advice. Captive insurance structures involve significant regulatory, actuarial, and financial considerations. Consult qualified advisors before making any captive-related decisions.