A practical guide for Missouri business owners on replacement cost, coinsurance penalties, and business interruption coverage

Missouri's severe weather season does not ask whether your insurance program is ready. Hail storms, tornadoes, and straight-line wind events have caused billions in commercial property losses across the state in recent years, and the claims that go wrong are rarely the result of bad luck alone. They are the result of coverage decisions that were made years earlier and never revisited.

The most damaging gap in most commercial property programs today is not a missing coverage line. It is an insured value that no longer reflects what it actually costs to rebuild. When that gap is exposed during a loss, it triggers a chain of financial consequences that business owners often do not anticipate until it is too late to do anything about them.

This article walks through the specific questions Missouri business owners should be asking about their commercial property coverage, and what the answers actually mean for your business.

What Happens If Your Business Is Underinsured?

When a building is insured below its actual replacement cost, several things can happen during a claim:

- Coinsurance penalties can reduce claim payments

- Policy limits may cap the total payout, even with replacement cost coverage

- Business interruption coverage may not reflect current revenue levels

- Out-of-pocket rebuilding costs increase significantly

In practice, this means that even when a loss is fully covered by the policy, the claim payment may still fall short of what it actually costs to repair or rebuild.

Why Building Values Become Outdated

Commercial construction costs in Missouri have increased significantly over the past several years. Labor shortages, supply chain disruptions, and rising material costs, especially for steel, lumber, and roofing systems, have pushed commercial rebuilding costs significantly higher than they were even three to five years ago.

Yet most commercial property policies are renewed annually with the same building values that were established at inception. Unless a business owner or their advisor specifically requests a revaluation, those numbers often sit unchanged for years. The result is a widening gap between what a building is insured for and what it would actually cost to rebuild it today.

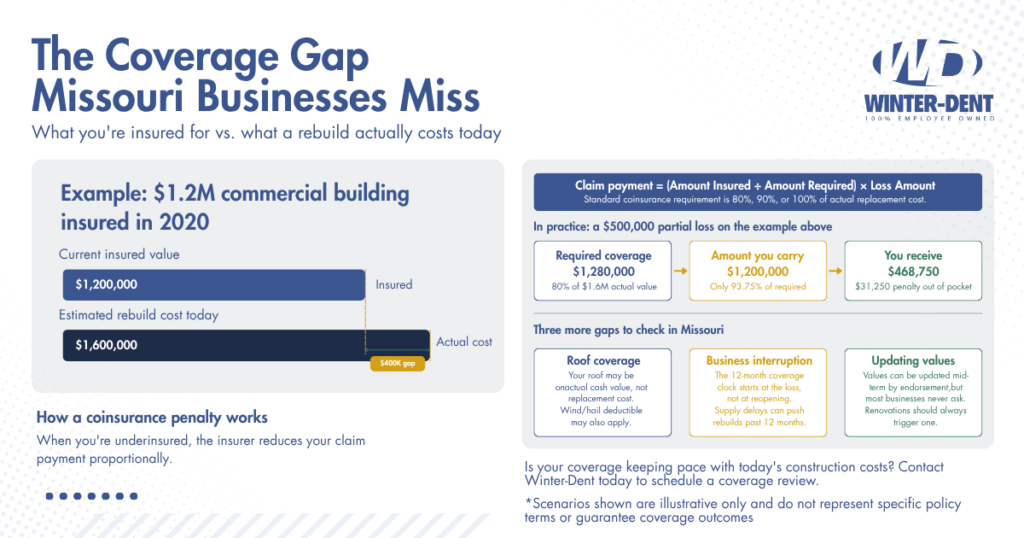

That gap is not a minor rounding difference. On a $1 million building, a 20 to 25 percent undervaluation is not unusual in today's market. That translates to $200,000 to $250,000 that your policy will not pay, regardless of how severe the damage is.

What construction cost escalation looks like in practice:

- A warehouse insured at $1.2 million in 2019 may cost $1.6 million or more to rebuild today

- HVAC, electrical, and fire suppression systems have seen some of the sharpest cost increases

- Specialized build-outs, including clean rooms, cold storage, or food processing environments, often escalate faster than general construction

- After major regional storm events, rebuilding demand can exceed contractor capacity, which often drives temporary spikes in labor and material pricing.

What Is a Coinsurance Penalty and How Does It Actually Work?

Coinsurance is one of the most misunderstood provisions in commercial property insurance, and it is the primary mechanism through which underinsurance becomes a tangible financial penalty at the time of a claim.

Here is the core concept: most commercial property policies require you to insure your building to a minimum percentage of its actual replacement cost value, typically 80, 90, or 100 percent. If you fall below that threshold, the insurance company does not simply pay your claim at face value. They apply a formula that reduces the claim payment proportionally.

The Coinsurance Formula

The calculation works like this:

| Claim Payment = (Amount Insured / Amount Required) x Loss Amount |

In practical terms: if your building would cost $2 million to replace today and your policy requires 80 percent coverage ($1.6 million), but you are only insured for $1.2 million, you are only 75 percent of where you need to be. A $500,000 loss would result in a claim payment of $375,000 rather than $500,000. You absorb the remaining $125,000 out of pocket.

This reduction applies to partial losses as well as total losses. Business owners often assume the coinsurance clause only comes into play if the building is a total loss. It does not. A significant roof claim, structural damage, or fire loss to one portion of the building is subject to the same formula.

Key coinsurance facts:

- 80/90/100 percent coinsurance requirements are standard on most commercial property forms

- The penalty applies to partial losses, not just total losses

- During a claim, the insurer and adjuster evaluate the building's actual replacement cost using construction cost data and valuation tools. That value is then used to determine whether the coinsurance requirement has been met.

- A coinsurance clause in your policy does not mean you were warned at renewal that you were underinsured

Does Replacement Cost Coverage Really Cover Today's Construction Pricing?

Replacement cost value (RCV) coverage is frequently cited as the standard for commercial property insurance, and for good reason: it covers the cost to rebuild without deducting for depreciation. But replacement cost coverage only pays up to the insured limit. If your insured value has not kept pace with construction cost increases, RCV endorsements do not fill the gap.

This is a distinction that matters. Replacement cost coverage tells you how the loss will be measured. Your insured limit tells you the ceiling on what the policy will pay. A policy with replacement cost coverage and an outdated insured value still results in an out-of-pocket shortfall when a significant loss occurs.

Some policies include an inflation guard endorsement, which automatically increases insured values by a set percentage each year. This can help maintain pace with general cost increases, but it is not a substitute for a proper appraisal. Blanket inflation adjustments do not account for the specific characteristics of your building, your location, or cost escalation in your industry.

The only reliable way to confirm your insured values are adequate is to have a replacement cost appraisal performed by a qualified professional, and to revisit that appraisal on a regular cycle.

Common Coverage Assumptions vs. Policy Reality

| What Many Owners Assume | What the Policy Often Says |

| Replacement cost means full rebuild at today's prices | RCV applies only up to insured value; if values are outdated, you carry the gap |

| Business interruption pays until we're back to normal | Coverage period is typically 12 months; extended period of indemnity may be limited |

| Our roof is fully covered | Wind/hail exclusions or ACV (actual cash value) limitations may apply |

| We can update our building value anytime | Endorsement changes mid-term are possible but not automatic; many owners never request them |

| Coinsurance only applies to older or small policies | Coinsurance clauses are standard on most commercial property forms, regardless of business size |

Roof Exclusions in Missouri: What Business Owners Often Miss

Missouri sits squarely in a corridor of severe convective storm activity, which means hail and wind losses are among the most frequent commercial property claims in the state. It also means that many insurers writing commercial property in Missouri have introduced policy language that limits how roof damage is handled.

Two provisions are particularly common and frequently misunderstood.

Actual Cash Value on Roofs

Even when a policy is written on a replacement cost basis for the building overall, the roof may be separately scheduled on an actual cash value (ACV) basis. Under ACV coverage, the insurer deducts depreciation based on the roof's age, condition, and expected useful life, which can significantly reduce the claim payment compared with the cost to install a new roof. A roof that is 15 years old may receive a settlement significantly less than what replacement actually costs, regardless of what the replacement cost provision says for the rest of the building.

Wind and Hail Exclusions or Sub-Limits

Some commercial property policies in Missouri now include separate deductibles for wind and hail losses, often expressed as a percentage of the building value rather than a flat dollar amount. On a $1.5 million building, a 2 percent wind and hail deductible means $30,000 comes out of your pocket before coverage applies. These provisions are not always clearly highlighted at renewal and can represent a significant change from prior policy terms.

In higher-risk areas or for buildings with older roofing systems, some carriers have moved to excluding wind and hail damage altogether or applying sub-limits that fall well short of actual replacement cost for roofing. Business owners in Missouri should ask specifically about how their roof is covered, not assume it mirrors the rest of the building.

Questions to ask your advisor about roof coverage:

- Is the roof covered on a replacement cost or actual cash value basis?

- Is there a separate wind or hail deductible, and how is it calculated?

- Are there any exclusions or sub-limits that apply specifically to roofing materials?

- When was the last time the roof's coverage terms were reviewed against the current policy form?

How Long Does Business Interruption Insurance Pay After a Storm?

Business interruption (BI) insurance is designed to replace lost revenue and cover continuing expenses when a covered property loss prevents normal operations. For most businesses, the question is not whether they have BI coverage but whether the coverage they have reflects the realities of a major storm recovery.

There are three dimensions of BI coverage that business owners frequently underestimate.

The Period of Indemnity

Most BI policies specify a period of indemnity, typically 12 months, during which covered losses are paid. This clock starts at the date of loss, not the date you reopen. If your building requires 10 months to rebuild, you have two months of BI coverage remaining to support revenue recovery after reopening. For businesses with longer recovery curves, that may not be enough.

Supply chain disruptions and contractor availability following a widespread weather event can extend rebuild timelines significantly. Following major tornado events in Missouri, restoration contractors are often booked out for months, and specialized building components can face lead times that were not anticipated when the policy was written.

Extended Period of Indemnity

Some policies include an extended period of indemnity endorsement, which provides coverage for the revenue shortfall after reopening while the business works back to pre-loss revenue levels. This endorsement is not standard on all policies, is frequently limited to 30 or 60 days, and is often overlooked entirely during renewal discussions.

For businesses that depend on customer relationships, established supply chains, or foot traffic patterns, the road back to pre-loss revenue can take considerably longer than the time required to physically reopen.

The Monthly Limit and Aggregate

Many BI policies include monthly limits or maximum periods of indemnity in addition to the overall policy limit. If your monthly BI limit was set based on revenue figures from several years ago and your business has grown, the monthly cap may not reflect what you are actually losing during a closure. Revisiting BI limits at renewal, based on current revenue and expense data, is as important as revisiting building values.

| Phase | What BI Typically Covers | Watch For |

| Waiting Period (Day 1-3) | No coverage yet; retention period applies | Some policies have 24-72 hour waiting periods before BI triggers |

| Active Restoration (Month 1-12) | Lost revenue + continuing expenses during rebuild | Period of indemnity clock starts at loss, not at reopening |

| Extended Indemnity Period | Revenue shortfall after reopening as business rebounds | Often capped at 30-90 days; many policies omit this entirely |

| Beyond Policy Period | Not covered | Supply chain delays and contractor backlogs can push rebuilds well past 12 months |

Can You Update Insured Values During the Policy Term?

This is a question business owners rarely think to ask, and the answer matters. Insured values can be updated mid-term through a policy endorsement. The change is prospective and takes effect from the endorsement date, not retroactively to the start of the policy term. But the option exists, and most businesses never use it.

The more common pattern is that values are reviewed once at renewal, adjusted modestly if at all, and then left unchanged for the following twelve months. If construction costs shift materially during the policy year, or if a business completes a renovation, builds an addition, or installs significant new equipment, those changes can create a coverage gap that persists until the next renewal.

A few practical points worth knowing:

- You can request a mid-term endorsement to increase insured values; the premium adjustment is calculated on a pro-rata basis for the remaining policy term

- Mid-term decreases in coverage may have different implications and should be reviewed carefully

- Any significant capital improvement to a building should trigger a conversation with your advisor about whether insured values need to be updated

- Maintaining documentation of building improvements, equipment purchases, and renovation costs makes it easier to demonstrate the appropriate insured value at renewal or in the event of a claim

What Good Broker Service Looks Like Before the Storm

The coverage gaps described in this article are not new problems. Coinsurance clauses, ACV roof provisions, and outdated building values have been features of commercial property insurance for decades. What changes is whether your advisor is actively monitoring them on your behalf or leaving that work to you.

Property insurance programs that are not actively reviewed tend to drift out of alignment with real-world rebuilding costs over time.

The difference between adequate service and genuinely proactive advisory service becomes most visible when a claim is filed. An advisor who surfaces these issues at renewal, walks you through the implications of your current insured values, and flags changes in your policy form from the prior year is providing a fundamentally different level of service than one who simply binds renewal and moves on.

At Winter-Dent, the Prevent365 process is built around exactly this kind of structured, ongoing review. Rather than treating renewal as a transaction, we use it as an opportunity to pressure-test your property program against current construction costs, review BI limits in light of your actual revenue, and evaluate whether your policy terms have shifted in ways that affect your exposure.

That work does not guarantee that every claim goes perfectly. But it does mean that when a storm hits, you are not discovering coverage limitations for the first time while standing in a damaged building.

What a structured property review should include:

- A comparison of current insured values against today's estimated replacement cost

- A review of BI limits against current revenue and realistic rebuild timelines

- A plain-language explanation of any coinsurance requirements in your policy

- Identification of ACV provisions, sub-limits, or exclusions that apply to roofing

- A summary of any policy form changes from the prior year that affect your coverage

- Documentation to support the insured values carried on the policy

Questions to Ask Before Severe Weather Season

Missouri's spring and summer storm season creates a natural moment to revisit these questions, but the right time to address coverage adequacy is before a loss occurs, not after. The following questions are worth putting directly to your insurance advisor:

- When were our building values last independently appraised, and how have construction costs changed since then?

- Does our policy include a coinsurance requirement, and are we currently meeting it?

- How is our roof covered, and does the policy apply ACV or replacement cost to roofing claims?

- Does our business interruption limit reflect current revenue, and is our period of indemnity long enough to cover a realistic rebuild scenario?

- Are there wind or hail deductibles or exclusions in our current policy that were not in place at our prior renewal?

- If we need to update our insured values, what does that process look like and what does it cost?

These are not complicated questions. But they require an advisor who has reviewed your policy thoroughly enough to answer them specifically rather than in generalities. If you are not confident that your current program has been evaluated at that level, that is itself important information.

FAQ: Commercial Property Underinsurance

What happens if a building is underinsured?

If a building is insured below its required replacement value, a coinsurance penalty may reduce the claim payment. The business may also face out-of-pocket rebuilding costs beyond the policy limit.

Does replacement cost coverage guarantee full rebuilding costs?

No. Replacement cost coverage determines how losses are measured, but the policy still only pays up to the insured limit carried on the building.

What is a coinsurance clause in property insurance?

A coinsurance clause requires the insured to carry a minimum percentage of the building's replacement cost, often 80%, 90%, or 100%. If the building is insured below that level, claim payments may be reduced proportionally.

| Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Policy language, coverage limits, and claim outcomes vary by insurer and policy form. Businesses should consult a licensed insurance professional to review their specific coverage and risk exposures. The scenarios and examples in this article are provided for educational purposes and are illustrative only. They do not represent specific policy terms or guarantee coverage outcomes. Insurance policy language, coverage limits, and applicable provisions vary. Consult a licensed insurance professional to review your specific policy terms and coverage adequacy. |