A practical look at why general liability is one of the most common lines inside captives, what retention levels make sense, and when GL belongs in the traditional market instead.

Yes, general liability can be placed in a captive structure, and it is one of the most frequently included lines in group and single-parent captives. GL works well inside captives because it generates predictable frequency in the working layer, rewards companies with strong loss control, and pairs cleanly with workers' compensation and auto in multi-line programs. Feasibility depends on loss ratio, claim severity profile, industry classification, and the company's ability to fund retained losses.

Why General Liability Is a Common Captive Line

General liability fits the captive model well for a simple reason: most GL losses are frequency losses, not severity losses. Slip-and-falls, minor property damage, small bodily injury claims, and routine premises incidents tend to settle within predictable ranges. Captives are designed to retain exactly that kind of working-layer loss, where actuarial projections are credible and member discipline drives outcomes.

GL also rewards the behaviors that captives are built around:

- Documented safety procedures

- Regular training and inspection cadence

- Fast claim reporting and active management

- Vendor and contractor controls

- Strong incident review and root cause analysis

Companies that take these seriously generally outperform their loss picks. In a traditional policy, that outperformance subsidizes the carrier's book. In a captive, it returns to the company as underwriting profit and investment income.

What Retention Levels Are Typical for GL in a Captive

Retention is the amount of loss the captive absorbs before reinsurance attaches. For general liability, retentions are calibrated to capture the frequency layer where members can influence outcomes through prevention.

Direct answer: Most group captives retain general liability losses between $100,000 and $500,000 per occurrence, typically structured in two tiers. The A fund handles smaller claims (often the first $100,000) and is funded by each member individually. The B fund pools losses above the A fund up to the captive's full retention, where members share risk together. Reinsurance attaches above the captive retention, with excess and umbrella layers placed in the traditional market.

A common GL structure inside a group captive looks like this:

| Layer | Range | Who Pays |

| A Fund (frequency) | $0 to $100,000 per occurrence | Member individually |

| B Fund (severity) | $100,001 to $500,000 per occurrence | Captive members pool |

| Reinsurance | $500,001 to $1,000,000 | Reinsurer |

| Excess / Umbrella | Above $1,000,000 | Traditional market |

Retention selection depends on:

- The member's loss frequency and average claim size

- Industry hazard classification

- Available reinsurance capacity

- The captive's surplus and operating history

- The company's cash flow tolerance for variability

Higher retentions generate more potential premium savings in good years but expose the company to more variability in bad ones. The right retention is the one that matches both the loss profile and the company's financial appetite.

What Claim Frequency and Severity Profile Makes GL Viable

Not every GL exposure fits a captive. The companies that succeed with GL in a captive share a recognizable profile.

Direct answer: GL is viable for captive inclusion when a company has predictable claim frequency, manageable severity, a five-year loss ratio under 60 percent, and clear evidence that safety and operational controls drive outcomes. Companies with sporadic but catastrophic GL exposure (large products liability verdicts, mass-tort potential, high-hazard premises) are typically better served by traditional placement or excess-only captive participation.

What captive underwriters look for:

- Steady claim frequency that supports actuarial credibility

- Average claim severity well within the proposed retention

- Few or no shock losses in the past five to seven years

- Industry classification that does not carry mass-tort or class-action exposure

- Strong contractual risk transfer (indemnification, additional insured status, hold-harmless agreements)

- Documented safety, training, and incident review programs

- Clean loss runs with detailed cause coding

What raises concern:

- Severity claims that have pierced or approached typical retention levels

- Industries with elevated products liability or completed operations exposure (certain manufacturers, construction trades with long-tail exposure)

- Operations in venues with extreme verdict patterns

- Weak vendor and subcontractor risk management

- Loss runs with vague cause coding or inconsistent reporting

GL feasibility is less about size than about pattern. A mid-market company with disciplined loss control and a clean five-year history is often a better candidate than a much larger company with one or two unresolved severity claims.

How Reinsurance Layers Over GL Inside a Captive

Reinsurance is what makes a captive financially safe. It caps the captive's exposure to severity losses that would otherwise drain surplus or trigger member assessments. For GL, reinsurance typically attaches at the top of the captive's retention and runs up to a defined limit, where the traditional umbrella or excess market takes over.

The structure usually has three protective layers above the working retention:

- Specific reinsurance. Covers individual losses that exceed the captive's per-occurrence retention. If the captive retains the first $500,000 of a GL claim, the reinsurer pays losses above that point up to the reinsurance limit.

- Aggregate stop-loss. Caps the captive's total annual loss exposure. If members collectively experience an unusually heavy year, the aggregate stop-loss protects the captive's surplus and prevents large member assessments.

- Excess and umbrella. Sits above the reinsurance layer in the traditional market and provides catastrophic protection at high limits, where capacity is deeper and pricing more efficient.

This layered structure is what allows a captive to retain meaningful GL premium without taking on catastrophic risk. It is also why captive underwriters scrutinize the loss profile so carefully. The reinsurance layer is priced based on what the captive is expected to absorb below it.

When Should General Liability Remain Fully Insured?

A captive is not the right answer for every GL exposure. There are clear cases where keeping GL in the traditional market is the better strategic decision.

GL should remain fully insured when:

- Loss ratios are above 70 percent or trending upward

- Severity claims are frequent enough that they would regularly pierce typical captive retentions

- The business operates in a high-hazard products or completed operations category

- Cash flow cannot absorb the variability of self-insured retentions

- The company is in a venue or industry segment with extreme nuclear verdict exposure

- Safety culture and documentation are still developing

- The total GL premium is small enough that captive overhead would erode the savings

The principle is the same as with any line: a captive does not change the underlying risk. It changes who funds the loss. A GL exposure that is volatile or catastrophic in the traditional market remains volatile or catastrophic inside a captive, just on the company's own balance sheet.

What Most Companies Do vs. What Proactive Companies Do

| What Most Companies Do | What Proactive Companies Do |

| Treat GL as a commodity coverage | Treat GL as a measurable cost center |

| Renew with the incumbent each year | Benchmark loss ratios against industry data |

| Address claims as they happen | Run quarterly trend reviews and adjust controls |

| Buy GL based on premium quote | Evaluate GL based on total cost of risk |

| Leave contractual risk transfer to legal | Coordinate insurance and contracts together |

| Keep all lines in the traditional market | Evaluate each line for captive feasibility on its own merits |

The proactive approach is what creates the loss ratio and documentation profile captive underwriters want to see. It is also what compounds savings inside a captive once a company qualifies.

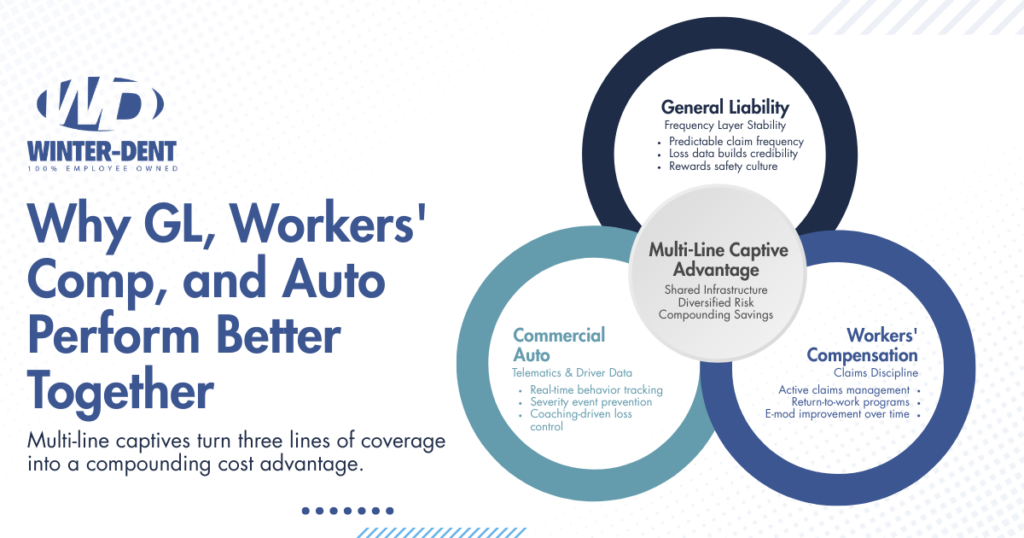

Strategic Insight: GL Often Performs Best in a Multi-Line Captive

GL alone produces savings, but GL inside a multi-line captive (alongside workers' compensation and commercial auto) typically produces more. Three reasons:

- Diversification stabilizes results. GL frequency, workers' comp severity, and auto volatility do not all move in the same direction. Bundling them smooths year-over-year variability.

- Shared infrastructure spreads cost. One actuarial review, one captive manager, one claims protocol, one reinsurance program. Overhead per line of coverage drops as more lines are added.

- Risk control synergies compound. The same operational discipline that reduces workers' comp claims usually reduces GL incidents too. Investments in safety, training, and incident review pay off across multiple lines.

For most mid-market companies, the strategic question is rarely "should GL go in a captive?" It is "if we are building a captive program, where does GL sit within it?" That question opens up better answers.

This is the kind of multi-year planning Prevent365 is built around: aligning safety performance, loss data, and captive structure so the program compounds value rather than starting over each renewal.

What This Means for Missouri Business Owners

Missouri businesses face the same national GL pressures (rising defense costs, social inflation, expanding plaintiff theories) along with state-specific factors like venue patterns in Jackson, St. Louis, and Greene counties, and industry concentrations in manufacturing, distribution, healthcare, and construction. The captive structures available to Missouri-based companies are the same as those available nationally, but the local underwriting story matters. Demonstrable safety performance, clean loss runs, and disciplined contractual risk transfer give Missouri companies more strategic options when evaluating GL placement.

Talk Through Your GL Strategy Before the Next Renewal

If you are wondering whether general liability belongs in a captive (or whether your current GL program is structured for long-term cost control) the right time to evaluate is well before renewal. Winter-Dent works with companies to assess captive feasibility, model retention scenarios, benchmark loss performance, and build the safety and documentation infrastructure that makes GL programs perform over the long term.

Reach out to Winter-Dent & Company to start a conversation about your GL strategy.

Disclaimer: This article is for educational purposes only and does not constitute insurance, legal, or financial advice. Captive insurance structures, retention levels, and feasibility criteria vary by program, jurisdiction, and individual company circumstances. Companies considering a captive should consult qualified advisors before making placement decisions.