A cyber policy is necessary, but it is not a strategy. Here is why business leaders who treat it as one are most exposed.

Most business leaders we meet have already bought cyber insurance. Some have carried it for years. When we ask what their policy covers, the answer is almost always the same: "everything cyber." When we ask what their deductible is, what the sublimits look like, and what controls their carrier required at renewal, the room usually goes quiet.

This is the gap that defines the current cyber insurance market. Coverage exists. Premiums are being paid. But the policies on the shelf and the operations they are supposed to protect have drifted apart, and the businesses absorbing that drift are the ones who find out at the worst possible moment.

Cyber insurance is necessary. It is not, on its own, protection. Here is why, and what proactive companies are doing instead.

The False Confidence Cyber Insurance Creates

When you sign a cyber policy, you are buying a financial backstop for events you cannot fully prevent. That is valuable. The problem is what comes next. Most businesses, once they have a policy in place, stop investing in the operational changes that would have prevented the loss in the first place. The policy becomes a substitute for risk management instead of a complement to it.

Carriers know this, which is why the entire cyber insurance market has changed in the last three years. Coverage is tighter. Premiums are higher. Renewal applications are longer. And most importantly, claim payouts are getting smaller relative to the loss. The companies that struggle most are not the ones without coverage. They are the ones who assumed coverage was the answer.

Why is cyber insurance alone not enough to protect a business?

Cyber insurance pays for the financial consequence of a covered event, but it does not prevent the event, reduce the operational disruption, or guarantee a full payout. Most policies include sublimits, control requirements, and attestation clauses that reduce or deny claims when controls are absent. A policy works best as the last line of defense, not the first.

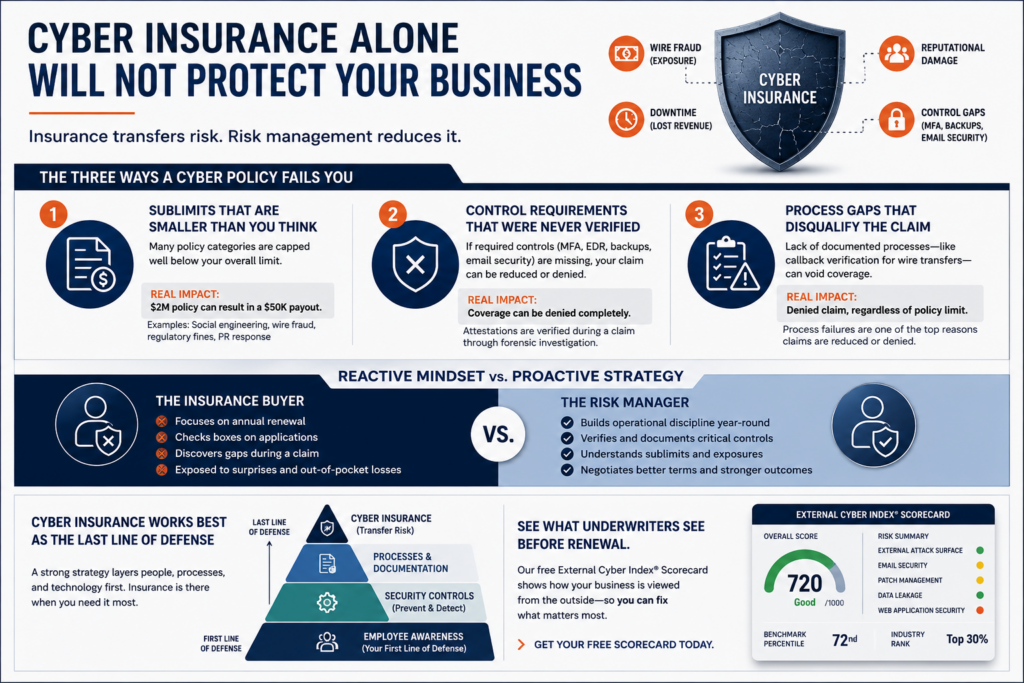

The Three Ways a Cyber Policy Fails You

When a cyber claim is reduced or denied, it almost always traces back to one of three issues.

1. Sublimits That Are Smaller Than You Think

A cyber policy with a $2 million limit does not mean $2 million is available for every kind of loss. Most policies break out specific categories of risk into sublimits, each capped well below the overall limit.

Common sublimits to look for:

- Social engineering fraud: Often capped at $50,000 to $250,000, even on multi-million-dollar policies.

- Funds transfer fraud: A common cap for wire fraud losses, especially without verification protocols.

- Regulatory fines and penalties: Frequently sublimited or excluded depending on jurisdiction.

- Reputational harm and PR response: Usually capped at a small fraction of the overall limit.

The most expensive cyber events for small and mid-sized businesses, including business email compromise and wire fraud, are exactly the events most likely to bump against a low sublimit. A million-dollar policy can produce a fifty-thousand-dollar payout, and the difference comes out of operating cash flow.

2. Control Requirements That Were Never Verified

Modern cyber policies are written on the assumption that certain controls are in place. Multi-factor authentication. Endpoint detection. Regular backups. Email authentication. The renewal application asks about each of these, and the insured signs an attestation that the answers are accurate.

The trouble starts during a claim. When a carrier opens a forensic investigation after a loss, they verify what was actually in place at the time of the incident. If MFA was promised on the application but missing on a critical email account, that gap can be the basis for a coverage denial. The market has shifted, and carriers are enforcing these terms.

The risk is not malicious misrepresentation. Most business owners answer the questions in good faith based on what their IT provider tells them. The problem is that "yes, we have MFA" can mean very different things in practice, and the gap between belief and reality is what shows up in a forensic report.

3. Process Gaps That Disqualify the Claim

Some categories of loss require not just controls, but documented processes. The most common example is funds transfer fraud. Most policies require callback verification of any banking change before a wire is sent. The verification has to be documented, the contact has to be at a known phone number, and the process has to be auditable.

If a company processes a wire based on an emailed instruction without calling the vendor back, and the wire turns out to be fraudulent, the carrier can decline the claim regardless of the policy limit. The exposure was insured. The process was not followed. The result is a denied loss.

The Conversation That Belongs on the Owner and CFO Desk

Cyber risk used to live inside the IT function. It does not anymore. Today, a cyber event creates exposure that lands squarely on leadership.

When a wire fraud loss hits, it does not show up on the IT director's P&L. It shows up on the operating cash flow report that the CFO presents to ownership. When a ransomware event triggers customer notification, regulatory filings, and a press response, the people answering those questions are the owners and the executive team, not the help desk.

There is a second, less obvious layer to this. Leadership has a growing fiduciary exposure around cyber decisions. Boards, partners, and lenders increasingly expect documented evidence that cyber risk has been assessed, addressed, and insured appropriately. "We trusted our IT provider" is becoming harder to defend as a leadership posture. The standard is no longer good faith. It is reasonable diligence.

For owners and CFOs, this changes the question entirely. The question is not whether cyber insurance is in place. It is whether the leadership team can demonstrate they understood the exposure, verified the controls, and matched the coverage to the actual risk. That is a documentation problem as much as a security problem, and it is one the broker should be helping solve, not the IT vendor.

What Most Businesses Do vs. What Proactive Businesses Do

| Reactive Approach | Proactive Approach |

| Treats cyber as an annual policy purchase | Treats cyber as a year-round operational risk |

| Trusts the IT provider to handle security | Verifies controls independently with documented evidence |

| Assumes the policy limit equals the payout | Reviews sublimits, retentions, and exclusions in detail |

| Discovers gaps during a claim | Discovers gaps during a pre-renewal assessment |

| Sees cyber as IT's problem | Sees cyber as a CFO, owner, and operations problem |

The difference is not size or industry. We have seen 30-person firms with stronger cyber posture than 300-person firms. The difference is whether cyber is treated as a year-round operational discipline or a once-a-year insurance line item.

The Strategic Insight Most Brokers Miss

Cyber insurance is not just a financial product. It is a feedback mechanism. The underwriting process is one of the most useful free diagnostics available to a business owner, because it forces a structured review of your controls, your processes, and your exposure.

The companies that get the most out of cyber insurance treat the renewal as a strategic moment, not an administrative one. They pre-empt the underwriter's questions with documented evidence. They enter the renewal with a third-party security rating already in hand, so they shape the conversation instead of being shaped by it.

Over a three-year cycle, the difference between a reactive renewal posture and a proactive one can be measured in tens of thousands of dollars of premium, broader coverage, and a far smaller loss when something does happen.

What is the difference between cyber insurance and cyber risk management?

Cyber insurance is a financial product that pays for the consequences of a covered event after it occurs. Cyber risk management is the ongoing operational discipline of preventing, detecting, and responding to cyber threats. Insurance transfers risk. Risk management reduces it. The two work together, and neither is sufficient on its own.

How Winter-Dent Approaches Cyber Risk

Winter-Dent treats cyber the way we treat every other commercial risk: as something to diagnose, differentiate, reduce, and only then insure. Our Prevent365 methodology applies four steps to cyber exposure.

Diagnose. We start with a complimentary external rating. It analyses your business on the same factors carriers and threat actors evaluate. A full assessment goes deeper into internal controls, vendor exposure, and incident response readiness.

Differentiate. We position your business to underwriters with documented controls, a clean submission, and a strong external rating. The goal is to be the easiest, cleanest account on the underwriter's desk, which is how better terms get earned.

Reduce. Phishing training, MFA verification, vendor payment protocols, patching cadence, and incident response planning lower both the probability and severity of a loss. We coordinate with your existing IT provider to close gaps.

Insure. Only after the first three steps is the policy structured. Coverage is matched to your actual exposure, with sublimits, retentions, and endorsements that reflect what could actually happen to your business.

Cyber insurance works best when it is the last line of defense, not the first.

What to Do Next

If your cyber policy is approaching renewal, or if you have been carrying coverage for more than a year without revisiting the sublimits, the highest-leverage thing you can do this quarter is talk to your Winter-Dent advisor about a cyber risk review.

In that conversation, we can walk through your current sublimits, flag any gaps that have opened up since your last renewal, and outline what underwriters are looking for right now.

Reach out to a Winter-Dent advisor to schedule a quick review, there is no obligation, and the insights are yours to use either way.

Frequently Asked Questions

If I have cyber insurance, why do I still need to invest in cybersecurity?

Cyber insurance pays for the consequences of an event after it occurs, but it does not prevent the event, replace lost time, or restore customer trust. Most policies also require specific controls and processes as conditions of coverage. Investing in cybersecurity reduces the chance of a loss, supports a stronger renewal submission, and ensures the policy will actually pay when needed.

What is the most common reason cyber insurance claims get denied?

The most common reasons are unmet control requirements, inaccurate attestations on the renewal application, and exceeding category sublimits such as funds transfer fraud or social engineering. A claim is rarely denied because the event was excluded entirely. It is reduced or denied because a required control was missing or a sublimit applied that the insured did not realize was in place.

How much cyber insurance does a small business actually need?

There is no universal answer because the right limit depends on industry, data sensitivity, transaction volume, vendor exposure, and regulatory profile. A common starting point for small to mid-sized businesses is $1 million to $5 million in overall limits, but the more important question is how that limit is structured. A $2 million policy with a $50,000 social engineering sublimit may leave you more exposed than a $1 million policy with broader category limits.

Does my IT provider's insurance cover my business if they cause a breach?

Sometimes, but rarely to the extent business owners assume. Most IT providers carry their own errors and omissions and cyber liability coverage, but those policies protect the provider, not the client. They typically respond only to direct negligence claims, often with sublimits and exclusions that leave the client absorbing significant losses. Your own cyber policy is the primary line of defense.

Can leadership be held personally liable for a cyber incident?

In most cases, the business entity absorbs the direct loss, but leadership exposure is growing. Boards, lenders, partners, and regulators increasingly expect documented evidence that cyber risk was assessed and addressed. Inadequate diligence can support claims of breach of duty, particularly in events involving customer data or financial fraud. Documenting the assessment, controls, and coverage decisions is the strongest protection.