A practical guide for business owners evaluating captive insurance as an alternative to the traditional market.

If you have been researching captive insurance, you have likely encountered a compelling picture: more control over your coverage, the chance to build equity through disciplined risk management, and freedom from the traditional insurance market's pricing swings. That picture is accurate. But evaluating a captive properly also requires understanding the downside.

What happens in a bad year? What if claims spike? Who absorbs the loss, and how far can that loss go?

These are the right questions to ask. And the answers, when explained clearly, are actually one of the strongest arguments for a well-structured captive arrangement. The key phrase being: well-structured.

This article walks through how captive insurance programs are built to handle adverse loss years, what the financial mechanics look like in practice, and what separates programs that hold up under pressure from those that do not.

What Happens If a Captive Has a Bad Year?

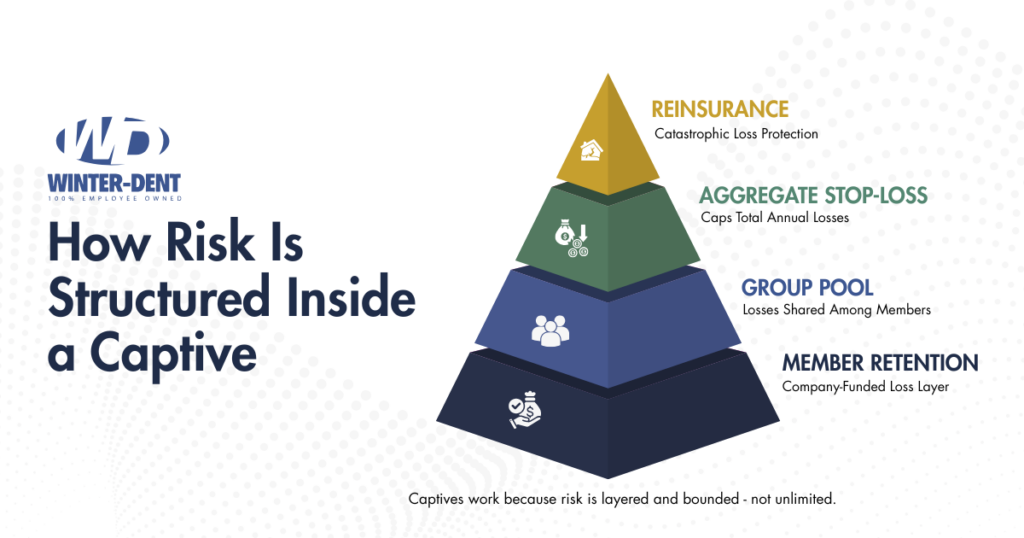

In a captive insurance program, a bad loss year means the captive’s funded loss reserves are used to pay claims, rather than an outside insurance carrier absorbing the cost.

However, well-structured captives include several safeguards designed to prevent a single bad year from destabilizing the program:

- Defined retention layers that limit member exposure

- Reinsurance that caps catastrophic losses

- Pooling structures that spread risk across multiple members

- Actuarial oversight that ensures reserves remain adequate

The goal is not to eliminate volatility entirely, but to bound it within predictable financial limits.

How Losses Are Funded Inside a Captive

In a traditional insurance arrangement, you pay your premium, and the insurer handles claims. The funding model is straightforward, even if you have little visibility into how your money is used or how claims are ultimately settled.

Inside a captive, the structure is more transparent and more direct. Your business (or your group of businesses, in a group captive) funds a dedicated loss reserve from which claims are paid. That reserve is held within the captive for the benefit of the program and its participants. It earns investment income, it can be structured to minimize tax exposure, and over time, it reflects the actual loss experience of your operation.

The mechanics vary by captive structure, but a common model works like this:

- A portion of your annual premium equivalent is deposited into a funded loss layer controlled by the captive.

- Claims within a defined retention band are paid from this fund.

- The fund is audited, reported, and subject to actuarial review to confirm it is adequately sized for projected losses.

- Investment income generated on captive reserves can offset program costs over time.

This is meaningfully different from writing a check to an insurance carrier and hoping for favorable treatment at renewal. You have visibility into where the money sits, how it is performing, and how it responds to actual claims.

The challenge, of course, is that in a bad year your funded layer absorbs real losses. That is the nature of retained risk. The question is not whether that can happen, but how the program is designed to limit how far it goes.

The Role of Reinsurance: Where the Ceiling Gets Set

While captives retain a portion of risk, they do not operate without protection.

One of the most important structural elements in any captive arrangement is reinsurance. This is the mechanism that converts potentially unlimited loss exposure into a defined and capped risk layer.

Reinsurance works by having the captive cede a portion of its risk to a reinsurer. In exchange for a reinsurance premium, the reinsurer agrees to cover losses above a defined threshold. For the business owner evaluating a captive, this answers one of the most fundamental questions: how bad can it actually get?

| How Reinsurance Limits Downside Exposure Think of it this way: your captive retains the first layer of risk (say, the first $500,000 in losses for a given coverage line). Reinsurance sits above that layer and responds when losses exceed the retention. You are exposed to volatility within your retention, not above it. The reinsurance premium is a cost. But it is also a ceiling. |

Well-structured captive programs use reinsurance in several ways:

- Specific (per-occurrence) reinsurance limits exposure from any single large claim.

- Aggregate stop-loss reinsurance limits total losses across all claims in a given period, so a high-frequency bad year is also capped.

- Quota share arrangements allow the captive to share proportional risk with a reinsurer, smoothing volatility further.

The appropriate reinsurance structure depends on the captive's size, the lines of coverage it writes, and the risk appetite of the participants. Larger, more mature captives may retain more risk and purchase less reinsurance. Newer or smaller captives typically carry tighter reinsurance protections while they build reserve strength.

The critical point is that reinsurance is not an afterthought in a well-managed captive. It is a core design element that is negotiated and priced at inception and reviewed annually as part of the program's ongoing stewardship.

How Pooling Distributes Risk in Group Captives

Many business owners enter the captive market through a group captive arrangement rather than a single-parent captive. Group captives allow multiple companies, typically in the same industry or with similar risk profiles, to pool their risk and share in both the losses and the rewards of collective performance.

Pooling changes the risk dynamic in important ways. It prevents a single participant’s losses from destabilizing the entire program. A single company having a bad year does not necessarily mean the entire group has a bad year. Favorable performance from other members offsets adverse experience from any one participant.

The mechanics of risk sharing inside a group captive typically follow this general structure:

| Risk Layer | Who Absorbs It | Typical Mechanism |

| Individual member retention | The member company directly | Per-occurrence deductible or funded layer |

| Group pool layer | All members collectively | Loss sharing agreement based on funding percentage |

| Excess layer | Reinsurer | Reinsurance treaty negotiated by captive management |

| Catastrophic layer | Reinsurer / surplus lines market | Aggregate stop-loss or excess-of-loss treaty |

This layered approach means your exposure is real but bounded. You are not writing a blank check to cover a catastrophic loss in the pool. Your obligation is defined, and reinsurance limits the aggregate exposure of the entire group.

Pooling also creates a compelling incentive structure. Members who manage their risk well are rewarded. Members who allow losses to accumulate may face higher contribution requirements or, in some structures, eventually exit the group. This creates genuine peer accountability that does not exist in a traditional insurance arrangement.

How Downside Exposure Is Structured

The word "downside" is worth taking seriously in any captive evaluation. Business owners considering a captive need to understand not just the upside potential, but the specific financial obligations that arise in an adverse scenario.

Here is how downside exposure is typically structured and bounded in a sound captive program:

Defined Retention Limits

Your financial obligation within the captive is tied to your defined retention, which is established actuarially based on your loss history, industry benchmarks, and the structure of the program. You know in advance what you are on the hook for within the retention layer.

Letter of Credit or Collateral Requirements

Group captives typically require members to post collateral, often in the form of a letter of credit, to cover their potential obligations within the program. This collateral is sized to reflect your retained exposure. It is not a premium payment that disappears; it is a financial commitment that can be released as losses develop favorably over time.

Collateral typically declines over time as claims mature and reserves are released.

Assessment Rights and Limitations

In some group captive structures, members can be assessed for additional contributions (beyond their originally funded loss layer) if the pool experiences losses beyond funded reserves. Sound programs define assessment rights clearly, cap them, and require reinsurance at levels that make catastrophic assessments unlikely. Before joining any group captive, you should understand exactly what the assessment mechanics are.

Actuarial Adequacy Reviews

Regulated captive programs require actuarial opinions confirming that reserves are adequate. This is not optional bureaucracy. It is the mechanism that catches underfunding before it becomes a crisis. A captive that routinely passes actuarial review with adequate reserves is a captive that has the financial depth to absorb a bad year without threatening members.

| The Question Every Business Owner Should Ask Before entering any captive arrangement, ask your advisor to walk you through a loss stress-test scenario: what does the program look like if we have a loss year that is 150% of our expected losses? What does my specific financial obligation look like? Where does reinsurance respond? A well-managed program should be able to answer those questions with specifics, not generalities. |

What Long-Term Performance Typically Looks Like

Captive insurance programs are not short-term strategies. They are built on multi-year actuarial assumptions, and their economic advantages compound over time as reserves grow, investment income accumulates, and underwriting performance stabilizes.

A single bad year inside a well-funded captive is rarely a crisis. It is a data point. The program absorbs the loss from reserves, reinsurance responds above the retention, and the following year begins the process of rebuilding reserve strength.

Over a full underwriting cycle, businesses in well-managed captives typically experience:

- Total cost of risk that trends lower than the traditional market, even accounting for bad years, because profitable years generate real returns.

- Greater stability in program costs, since pricing is driven by your own loss experience rather than market-wide loss trends.

- Accumulated reserves that represent actual equity in the program, rather than premiums paid and gone.

- Improved claims management, because both the captive structure and peer accountability create incentives to close claims efficiently and reduce severity.

What long-term performance does not look like is a straight line. There will be years with elevated losses. The question is whether the program is designed to absorb them without permanent damage, and whether your business has the financial capacity to weather a short-term funding requirement without operational disruption.

This is why captive programs are not right for every business. Financial stability, adequate cash flow, and a genuine commitment to risk management are baseline requirements. Captives reward businesses that take risk control seriously. For many organizations, workers’ compensation is often the first coverage line evaluated for a captive structure. They are not a mechanism for businesses with poor loss histories to escape the consequences of that history.

What Separates Well-Managed Captives from Those That Struggle

Captive success is not determined by the concept of captive insurance itself, but by how the program is designed and managed.

Not all captive programs are created equal. The structure, governance, and ongoing management of a captive determine whether it performs as designed or creates unexpected financial stress for its members.

Captives that hold up under pressure share several characteristics:

- Strong reserves: Adequate capitalization from the start

- Realistic loss modeling: Conservative actuarial assumptions that do not assume the best-case scenario

- Disciplined reinsurance: Reinsurance that is appropriately structured for the captive's size and risk profile, renewed and reviewed annually

- Hands-on claims management: Active oversight of how claims are managed, not just how losses are funded

- Governance and transparency: Clear reporting, regular communication with members, and transparent disclosure of program performance

- Risk management orientation: A commitment to loss prevention that reduces the frequency and severity of claims in the first place

That last point deserves emphasis. The most effective captive programs treat loss prevention as a core function, not an afterthought. When members actively work to reduce workplace injuries, manage liability exposure, and control claims, the whole group benefits. The captive structure creates a direct financial incentive to do what businesses should be doing anyway.

Captives that struggle tend to share a different profile: underfunded from the start, lax in claims oversight, reliant on optimistic actuarial projections, and lacking the governance infrastructure to catch problems before they compound. These are not inherent flaws in the captive model. They are management failures that a qualified advisor and proper due diligence can help you avoid.

How Winter-Dent Approaches Captive Advisory

When Winter-Dent works with clients evaluating captive insurance, our Prevent365 methodology shapes every part of the analysis.

We do not start with the assumption that a captive is automatically the right answer. We start with a complete picture of your total cost of risk: your current loss trends, your risk management maturity, your cash flow capacity, and the specific exposures that drive your insurance spend.

That analysis tells us whether a captive is likely to perform for your business over a full underwriting cycle, not just in favorable years. It also tells us what risk management work needs to happen to give your captive program the best possible foundation.

For businesses that are a genuine fit, we walk through program structure in detail, including how losses are funded, where reinsurance sits, what your specific financial obligations look like in stress scenarios, and what governance should look like over the life of the program.

If the numbers and the structure make sense, we help you get there. If they do not, we tell you that clearly and focus on what will actually reduce your total cost of risk.

Frequently Asked Questions About a Bad Year Inside a Captive

The following questions reflect how business owners and financial leaders are researching captive insurance performance and risk management today.

Is a captive insurance program risky?

Captive insurance involves retaining a portion of risk rather than transferring it entirely to an insurer. However, well-structured captive programs use layered protections such as reinsurance, pooling arrangements, and actuarial oversight to limit downside exposure and ensure the program remains financially stable.

What happens to my money if I leave a group captive after a bad loss year?

Exiting a group captive after a bad year is more complex than exiting after a favorable one. Depending on your program's structure, you may be required to leave your funded reserves in the program for a defined tail period, typically three to five years, to allow claims from your participation period to fully develop and close. Some programs also include contractual provisions that adjust exit distributions based on your loss ratio relative to the group. Before entering any captive, review the exit terms carefully and understand the financial mechanics of departure under adverse conditions.

Can a captive insurance program go insolvent?

Yes, captives can become financially impaired or insolvent, though it is uncommon in properly structured and regulated programs. Insolvency typically results from a combination of underfunding, poor claims management, and inadequate reinsurance. Most captives domiciled in reputable jurisdictions are subject to regulatory reserve requirements and actuarial review processes designed to catch financial weakness before it reaches a crisis point. When evaluating a captive, review the program's domicile, its regulatory oversight structure, its actuarial certifications, and the financial strength ratings of its reinsurers.

How does aggregate stop-loss reinsurance protect captive members?

Aggregate stop-loss reinsurance sets a ceiling on the total amount of losses the captive (and its members) are responsible for during a defined policy period, regardless of how many individual claims occur. If total losses across the program exceed the aggregate stop-loss attachment point, the reinsurer covers the excess up to a defined limit. This protection is particularly valuable in high-frequency loss scenarios where no single claim is catastrophic, but the cumulative volume of claims could strain the captive's reserves. Aggregate stop-loss is one of the key mechanisms that prevents a bad year from becoming a program-threatening event.

How long does it typically take for a captive to build meaningful reserve strength?

Reserve accumulation depends on premium volume, loss experience, and how much the program retains versus cedes to reinsurance. In general, group captive participants begin to see meaningful reserve growth within three to five years of joining, assuming loss performance is at or below expected levels. Single-parent captives funded at higher premium volumes may build reserves more quickly. Investment income on the reserve fund also contributes to growth over time. The key point is that captive programs are multi-year financial commitments, not short-term arrangements, and the reserve-building phase requires patience and consistent loss management.

What risk management practices most directly improve captive performance?

Captive performance is driven primarily by loss frequency and severity. The practices that move the needle most directly include structured safety and loss prevention programs that reduce the incidence of claims, early intervention and return-to-work protocols for workers' compensation claims, rigorous claims reporting and oversight to ensure claims are managed efficiently and closed appropriately, regular review of contract language and liability exposure to avoid third-party claims, and consistent data collection that allows actuaries and program managers to identify emerging trends before they become problems. Businesses that treat these practices as operational priorities, not just insurance requirements, consistently outperform their peers inside captive programs.

Disclaimer: The scenarios and financial structures described in this article are illustrative and for educational purposes only. They do not constitute insurance or financial advice. Captive insurance programs involve retained risk and financial obligations that vary by program structure. Businesses should consult qualified risk and financial advisors before entering a captive arrangement.