The underwriting process has changed. If your renewal still feels like a formality, you may already be behind.

If your most recent insurance application felt longer, more invasive, and harder to answer than anything you have seen before, you are not imagining things. The underwriting process for Missouri businesses has fundamentally shifted over the past two years, and the questions carriers are asking today go well beyond revenue, payroll, and claims history.

Underwriters in 2026 are evaluating how your business actually operates. They want to see your internal controls, your safety documentation, your subcontractor agreements, your IT vendor relationships, and your fleet management data. They are not doing this to create busywork. They are doing it because the economics of commercial insurance have changed, and carriers can no longer afford to price risk based on industry averages and assumptions.

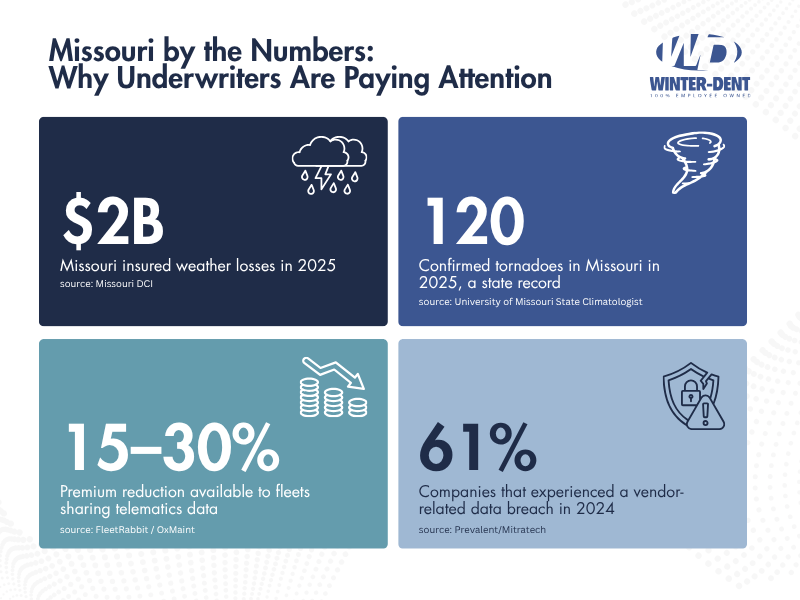

For Missouri businesses specifically, this shift is amplified by the state’s severe weather exposure, a highly competitive workers’ compensation market, and rising liability severity driven by social inflation. Missouri’s insured losses from severe weather events approached $2 billion in 2025 alone, and the state recorded 120 confirmed tornadoes that year. Underwriters are paying closer attention to Missouri accounts because the data demands it.

This article breaks down the questions underwriters are now asking, explains why each one matters, and shows you how to build the kind of risk profile that earns better terms, not just competitive quotes.

Why Underwriting Suddenly Got So Detailed

The short answer: underwriters are moving from backward-looking to forward-looking risk assessment.

For decades, commercial underwriting relied heavily on historical data. Your loss history, your industry class code, your revenue, and your years in business were often enough to generate a quote. The underwriter’s job was largely about pricing what had already happened and hoping the future looked similar.

That model has been significantly disrupted. Several forces collided at once:

- Social inflation and nuclear verdicts pushed casualty loss costs beyond what historical trends predicted. U.S. insurers added $16 billion to prior-year liability reserves in 2024 alone.

- Severe convective storm losses exceeded $50 billion globally in 2025, with Missouri among the hardest-hit states.

- Cyber threats evolved faster than annual applications could capture, making static questionnaires unreliable.

- AI-assisted underwriting tools gave carriers the ability to evaluate more data points, faster, which raised the baseline expectation for every submission.

The result is that underwriters now evaluate operational maturity, not just loss history. They want to understand how your business prevents losses, not just how many you have had.

Underwriting became more detailed because carriers shifted from pricing historical losses to evaluating operational risk controls. Social inflation, catastrophic weather losses, and AI-driven analytics now allow underwriters to assess how a business prevents losses, making internal controls, safety documentation, and vendor management central to the underwriting process.

The 7 Questions Underwriters Are Asking (And What They Are Really Evaluating)

1. “Tell us about your internal controls.”

This question is not about accounting. When an underwriter asks about internal controls in a commercial insurance context, they want to understand the systems, policies, and procedures you have in place to prevent losses before they happen.

That includes:

- Written safety policies and whether they are enforced, not just filed

- Documented training programs with attendance records and completion tracking

- Inspection checklists for equipment, facilities, and job sites

- Payment verification procedures and access controls (relevant to crime and cyber coverage)

- Incident reporting protocols and root cause analysis documentation

The underwriter is looking for maturity. They do not expect perfection. They expect clear ownership, consistent follow-through, and documented evidence that your business takes loss prevention seriously.

Businesses that can present organized safety records, training logs, and inspection documentation are signaling to the underwriter that their risk profile is more predictable. Predictability is what earns better pricing.

2. “Do you have formal safety documentation?”

This is related to internal controls but more specific. Underwriters increasingly want to see that safety programs exist in writing, are reviewed regularly, and produce measurable results.

A verbal safety culture is no longer sufficient. Carriers want to see:

- A written safety manual that is current and specific to your operations

- OSHA logs and injury tracking records (even in states where specific formats are not mandated)

- Job hazard analyses for high-risk tasks

- Return-to-work protocols for injured employees

- Documentation of corrective actions taken after incidents

The shift toward documented safety programs reflects a broader underwriting trend: carriers are using data-driven risk selection, and documentation is the data they rely on. An underwriter cannot give you credit for a strong safety culture if there is no evidence of it in your submission.

Formal safety documentation matters to underwriters because it provides verifiable evidence of loss prevention efforts. Carriers use documentation such as written safety manuals, OSHA logs, training records, and corrective action reports to assess operational maturity and predict future loss behavior. Businesses without this documentation face higher premiums or narrower coverage.

3. “What are your subcontractor agreements and insurance requirements?”

This question has moved from a construction-specific concern to a cross-industry underwriting priority. Any business that hires subcontractors, independent contractors, or third-party service providers is now being evaluated on how well it manages that transferred risk.

Underwriters want to know:

- Do your contracts require subcontractors to carry their own general liability, workers’ compensation, and commercial auto coverage?

- Do you collect and verify certificates of insurance before work begins?

- Are you listed as an additional insured on your subcontractors’ policies?

- Do your contracts include hold harmless and indemnification language?

- Do you have a system for tracking certificate expirations and renewals?

The reason this matters: if a subcontractor causes an injury or property damage and lacks adequate coverage, the claim often flows back to the hiring company. Underwriters have seen this pattern enough times that they now treat weak subcontractor management as a direct underwriting risk.

For Missouri businesses in construction, manufacturing, and property management, this is especially relevant. The state’s competitive workers’ compensation market (over 100 insurance groups and 340 underwriting companies actively writing workers’ comp in Missouri) means carriers have choices about which risks to accept. Businesses with sloppy subcontractor oversight are easier to decline.

4. “Does your business use third-party IT providers, and how do you manage that relationship?”

Cyber underwriting has moved from a niche specialty to a core component of the commercial submission. If your business relies on managed service providers, cloud platforms, or outsourced IT support, underwriters want to understand the risk those relationships introduce.

This is not just about whether you have a firewall. Underwriters are asking:

- Who has administrative access to your systems, and are those credentials managed separately from your internal accounts?

- Does your IT provider maintain their own cyber liability coverage?

- Do you have a written vendor management policy for technology providers?

- Are your backups controlled by you or entirely dependent on a third party?

- Have you tested your incident response plan, and does it account for a failure at your IT provider?

The underwriting logic is straightforward. 61% of companies experienced vendor-related breaches in 2024, up from 41% the prior year. Underwriters are not penalizing businesses for using outside IT. They are penalizing businesses that cannot demonstrate oversight of that relationship.

Many 2026 cyber policies now include AI-related exclusions, and underwriters are beginning to ask about hardware supply chain decisions and whether employees use unauthorized AI tools with company data.

5. “What fleet management and telematics data can you provide?”

Commercial auto remains one of the most challenging insurance lines in 2026. Claim severity continues to climb, driven by distracted driving, larger jury awards, and rising vehicle repair costs. Missouri businesses that operate fleets face particular scrutiny.

Underwriters are now asking specifically whether you use telematics, and if so, what the data shows. The questions typically include:

- Do you have GPS tracking and telematics installed across your fleet?

- Can you provide driver behavior scorecards (hard braking, speeding, following distance)?

- Do you use dash cameras, and are they AI-enabled for event detection?

- What is your driver coaching process when telematics flags risky behavior?

- Can you share 6 to 12 months of continuous telematics data?

The pricing impact is real. Fleets that share verified telematics data showing safety improvements are seeing 15 to 30 percent premium reductions at renewal. Carriers including Nationwide, Progressive, Travelers, and Sentry now offer formal telematics discount programs.

Conversely, businesses that operate commercial vehicles without any telematics or driver monitoring data are becoming harder to place. Some carriers have stopped quoting commercial auto entirely for accounts that cannot demonstrate a proactive safety program.

Telematics data directly affects commercial auto pricing in 2026. Carriers now offer 15 to 30 percent premium discounts for fleets that share verified driving behavior data, including hard braking rates, speeding frequency, and following distance compliance. Businesses without telematics data face higher rates and fewer carrier options.

6. “Walk us through your claims history and what you have done about it.”

This is not a new question, but the depth of what underwriters want has changed. A five-year loss run is table stakes. What underwriters now evaluate is whether you learned anything from your claims.

They want to see:

- Root cause analysis for significant losses

- Documented corrective actions taken after each claim

- Trend data showing whether claim frequency or severity is improving

- Evidence that loss patterns have been addressed operationally, not just financially

A business with three workers’ compensation claims in three years is a very different risk depending on whether those claims were random events or the result of the same unaddressed hazard. Underwriters are trying to distinguish between businesses that have bad luck and businesses that have bad systems.

7. “How has Missouri’s severe weather exposure affected your property and operations?”

This question reflects a Missouri-specific reality that national market outlooks often understate. Missouri’s weather-related insured losses have been significant and sustained.

In 2025 alone, Missouri recorded 120 confirmed tornadoes. An EF-3 tornado that struck St. Louis in May 2025 caused an estimated $1.6 billion in property damage. Statewide, insured losses from severe weather events approached $2 billion for the year. Severe convective storm activity across the central U.S. generated over $50 billion in global insured losses in 2025, and Missouri was among the more heavily impacted states in the central U.S.

For Missouri businesses, this means property underwriters are scrutinizing:

- Whether your property values reflect current replacement costs (not original purchase price or assessed value)

- Your roof age, condition, and material (hail and wind resistance)

- Business continuity and disaster recovery planning

- Whether you carry adequate business interruption coverage

- Flood exposure, particularly near major river systems

Underwriters are not asking these questions to deny coverage. They are asking because Missouri’s weather profile has made accurate property valuation and disaster preparedness essential to writing a sustainable book of business in the state.

What Most Missouri Businesses Do vs. What Proactive Businesses Do

| Area | Reactive Approach | Proactive Approach |

| Safety documentation | Verbal policies, created at renewal time | Written programs maintained year-round with training logs and inspection records |

| Subcontractor management | Collect COIs at project start, never follow up | Track expirations, verify limits, require additional insured status, enforce contract language |

| Cyber/IT vendor oversight | Assume the IT provider handles everything | Written vendor management policy, separate admin credentials, tested incident response plan |

| Fleet management | No telematics, react to accidents after they happen | Telematics with driver scorecards, coaching protocols, 6 to 12 months of continuous data shared at renewal |

| Claims response | File the claim, move on | Root cause analysis, corrective actions documented, trends tracked and presented to underwriter |

| Property valuation | Use original purchase price or tax assessment | Annual replacement cost review accounting for construction inflation, material costs, and code upgrades |

| Renewal preparation | Wait for the broker to call 30 days before renewal | Begin 90 to 120 days out, assemble documentation, build a submission narrative for the underwriter |

The Strategic Insight Most Businesses Miss

The shift in underwriting is not temporary. It’s a structural shift in how risk is evaluated. Carriers have invested heavily in data-driven risk selection, AI-assisted analysis, and predictive modeling. The days of getting a competitive renewal based primarily on relationships and market timing are fading.

What this means for Missouri business owners is that the submission itself has become a strategic document. The businesses that consistently get the best outcomes are not necessarily the ones with the fewest claims. They are the ones that present the clearest, most documented picture of how they manage risk.

This creates a compounding advantage. A business that builds strong safety documentation, tracks its claims data, manages subcontractor risk proactively, and invests in fleet telematics is not just answering underwriting questions better. It is actually reducing its exposure, which produces fewer claims, which further improves its underwriting position, which earns better terms.

The businesses that treat the underwriting process as a once-a-year scramble are stuck in a cycle of reactive positioning. The ones that treat risk management as an ongoing operational discipline are building durable cost advantages that compound year over year.

How Prevent365 Addresses What Underwriters Want to See

Winter-Dent’s Prevent365 methodology was built specifically to close the gap between how businesses actually manage risk and how underwriters evaluate that management.

Rather than treating insurance as a transaction that happens once a year at renewal, Prevent365 embeds risk management into your operations across every quarter. This is not a generic safety checklist. It is a structured diagnostic and advisory process designed to make your business more resilient and more underwritable at the same time.

Here is how Prevent365 directly addresses the underwriting questions covered in this article:

Internal controls and safety documentation.

Prevent365 uses tools like AutomateSafety and OSHAlogs to help Missouri businesses build and maintain the documented safety programs that underwriters now require. These are not one-time audits. They are ongoing systems that produce the training records, inspection documentation, and corrective action trails that differentiate your submission from the stack of incomplete applications on the underwriter’s desk.

Subcontractor and vendor risk management.

Prevent365 includes a structured review of your contractual risk transfer practices, certificate of insurance tracking processes, and additional insured requirements. The goal is to eliminate the gaps that underwriters flag and that create uninsured exposure for your business.

Fleet and telematics integration.

For Missouri businesses with commercial vehicles, Prevent365 helps connect your telematics data to your insurance strategy. This means working with your broker to package driver behavior data, coaching records, and safety trend reports in the format underwriters use to justify premium credits.

Claims analysis and trend reporting.

Through ModSure, Prevent365 provides loss analysis that goes beyond simple loss runs. You get root cause tracking, frequency and severity trending, and the ability to present your claims narrative in underwriting language, showing what happened, why, and what you changed.

Underwriter positioning.

The most important outcome of Prevent365 is that it transforms your renewal from a data dump into a strategic presentation. Instead of handing the underwriter a stack of forms and hoping for the best, you are showing them a documented, year-round risk management discipline that reduces their uncertainty about your account.

If your business is preparing for a renewal and you want to understand how your risk profile compares to what underwriters are looking for in 2026, Winter-Dent offers a no-obligation risk assessment through the Prevent365 framework. The goal is not to sell you a policy. It is to help you see your business the way an underwriter sees it, and then close the gaps before they cost you.

Frequently Asked Questions

How far in advance should a Missouri business start preparing for a commercial insurance renewal?

Begin at least 90 to 120 days before your renewal date. This gives you time to update property valuations, gather telematics data, compile safety documentation, verify subcontractor certificates of insurance, and build a complete submission package. For complex accounts with layered property programs, catastrophic weather exposure, or large commercial fleets, starting even earlier is advisable. The businesses that consistently get the best renewal outcomes are the ones that treat preparation as a quarter-long process, not a last-minute scramble.

Can a Missouri business negotiate better insurance terms even with a recent claims history?

Yes, but only if you can demonstrate what changed after the claims. Underwriters distinguish between businesses that have experienced losses and businesses that have unresolved loss patterns. Documented root cause analysis, corrective actions, trend improvements, and operational changes made in response to claims can significantly offset the impact of recent loss activity. The key is showing the underwriter that your risk profile has improved, not just that time has passed since the last claim.

What happens if my subcontractors do not carry the insurance my underwriter expects?

Your own premiums may increase, your coverage terms may tighten, or carriers may decline to quote your account. When subcontractors lack adequate general liability, workers’ compensation, or commercial auto coverage, the financial liability for their actions often flows back to the hiring company. Underwriters view weak subcontractor insurance requirements as a gap in your risk management program. In Missouri’s competitive market, where carriers have many options for which risks to write, this kind of gap can move your account from “preferred” to “substandard” classification.

Is telematics data required for commercial auto insurance in Missouri, or is it optional?

Telematics is not legally required, but it has become a practical necessity for competitive pricing. Carriers including Nationwide, Progressive, Travelers, and Sentry now offer formal telematics discount programs, with documented savings of 15 to 30 percent for fleets that share verified driving behavior data. Businesses that cannot provide telematics data are increasingly limited in which carriers will quote their commercial auto, and the quotes they do receive tend to reflect industry-average risk rather than their actual driving performance. For most Missouri businesses with five or more commercial vehicles, the cost of telematics systems is recovered through premium savings within the first year.

Are Missouri insurance carriers tightening underwriting standards more than carriers in other states?

Missouri faces a unique combination of pressures that make underwriting more selective in the state. Severe convective storm losses approached $2 billion in insured weather losses in 2025, and the state recorded 120 confirmed tornadoes that year. The workers’ compensation market is highly competitive, with over 100 insurance groups writing in Missouri, which gives carriers the ability to be more selective about which risks they accept. Missouri’s position in the shifting Tornado Alley corridor means property underwriters are paying closer attention to building condition, roof age, and disaster preparedness than they might in lower-exposure states. The tightening is not punitive. It is a direct response to the data.

This article is provided for educational and informational purposes. It does not constitute insurance advice. Coverage terms, conditions, and availability vary by carrier and by the specific details of each business. Consult with a lice